This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Treasuries Rally on Softer ADP Data

October 5, 2023

On Wednesday, US Treasuries reversed the sell-off seen a day prior as yields dropped by 11-12bp across the curve on the back of soft data. US ADP payrolls rose by only 89k in September, far below expectations of a 150k print and the lowest since January 2021. The ADP report also said that annual wage growth slowed to 5.9%, the twelfth consecutive monthly decline. However, it is to be noted that the ADP numbers can differ significantly from the NFP print later on Friday that is expected at 170k. Also, the US services sector grew albeit at a slowing pace as the ISM Non-Manufacturing PMI came at 53.6 in September vs. 54.5 in August. In credit markets, US IG CDS spreads were 1.2bp tighter while HY spreads tightened 7.7bp. US equities were higher with the S&P and Nasdaq up 0.8% and 1.4% respectively.

European equity markets ended mixed. In credit markets, European main CDS spreads were tighter by 0.1bp and crossover spreads tightened 1.4bp. Asian equity markets have opened higher this morning. Asia ex-Japan IG CDS spreads widened 0.6bp.

New Bond Issues

New Bond Pipeline

- Damac Real Estate hires for $ 3.5Y sukuk bond

- Oman Telecom hires for $ 7Y sukuk bond

- Uzbekistan hires for $ 5Y/10Y bond

- Philippines hires for $1bn Retail bond

Rating Changes

- Fitch Downgrades Volcan to ‘B-‘; Places on Rating Watch Negative

- Fitch Downgrades Groupe BPCE to ‘A’; Outlook Stable

- Moody’s downgrades Codelco’s ratings to Baa1; negative outlook

- Fitch Upgrades Rolls-Royce to ‘BB’; Outlook Positive

Term of the Day

Convertible Bonds

As the name suggests, convertible bonds are debt instruments issued by a company where the bonds can be converted into equity shares of the company by the bondholders at a particular ratio and at particular points in time. Thus, it is a hybrid security as it has characteristics of both debt and equity. Convertibles generally carry a lower coupons and sometimes tax advantages for the issuer.

Talking Heads

On Stocks ‘Clearly Overvalued’ as Bond Yields Rise – Bill Gross, former CIO of PIMCO

“I’d pass on stocks and bonds in terms of future total returns”… bonds are a “better deal” than equities in an economic slowdown or recession

“The intensification of the higher-for-longer narrative, along with the rise in oil prices, has also been the primary driver of broad U.S. dollar strength. The speed of the move has lead to weaker currencies within the region, a violent sell-off in local rates and wider EM credit spreads”

On EM Bond Yields Sending a Worrying Signal

Charles Robertson, head of macro strategy at FIM Partners

“The selloff in US bonds is where the risk is coming from – risk to US equities, risk to low-rated emerging-market credits, and indirectly, a risk for global equities. History is not telling us we should assume a big reversal in US yields… Pricing is nowhere near as extreme as in 2008-09, but EM bonds do become more attractive the higher US yields go”

On BOJ May Scrap Yield Control Later This Year – Pimco’s Global Economic Advisor, Richard Clarida

“If data indicate inflation can sustain more than the BOJ currently forecasts, which we expect, then the BOJ could abolish YCC late this year or early next… At some point, as the economy reflates, we expect the BOJ will move away from the zero or below-zero… policy rate could be hiked to 0% by early 2024”

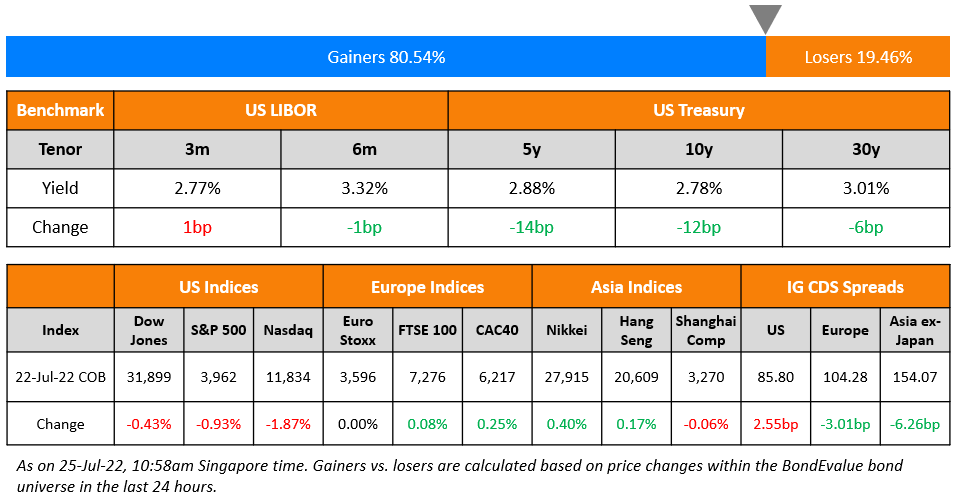

Top Gainers & Losers- 05-October-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.