This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Treasury Yields Rise After CPI Print; BBVA Prices € AT1 at 8.375%

June 14, 2023

US Treasury yields jumped higher by 8-10bp led by the 2Y and 5Y yields following the CPI print. US CPI for May 2023 rose by 4.0%, lower than expectations of 4.1% and the previous month’s 4.9%. Core CPI came at 5.3%, higher than expectations of 5.2%, and lower than the previous month’s 5.5%. The inflation print broadly saw markets confirming a Fed rate pause (94% probability) at today’s FOMC meeting whilst also reducing expectations of rate cuts later this year. For the July meeting, markets are pricing in a 61% probability of a 25bp rate hike. The peak Fed Funds Rate was 2bp lower at 5.29% for September. Equity indices ended higher with the S&P and Nasdaq up by 0.7-0.8%. US IG and HY CDS spreads tightened 0.7bp and 2.5bp respectively.

European equity indices closed higher too. European main CDS spreads were 0.7bp tighter and Crossover spreads tightened 2.5bp. Asia ex-Japan CDS spreads tightened another 1.9bp with Asian equity markets have opened mixed this morning.

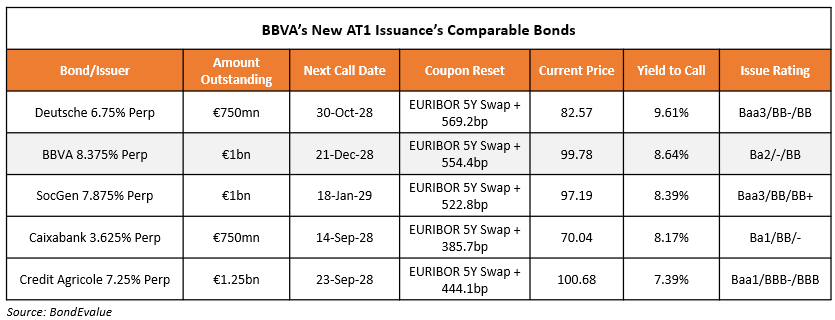

.png)

New Bond Issues

- Fujian Jinjiang Urban $ 364-Day at 6.3% area

BBVA raised €1bn via a PerpNC5.5 bond at a yield of 8.375%, 37.5bp inside initial guidance of 8.75% area. If the bonds are not called on their first call date of 21 December 2028, the coupon will reset then and every five years thereafter to the EURIBOR 5Y ICE swap rate plus a spread of 554.4bp. The bonds have expected ratings of Ba2/BB (Moody’s/Fitch). This is the first euro-denominated AT1 deal since the Credit Suisse AT1 write-off in March. The table below compares BBVA’s new AT1 with other similarly rated European AT1s. The notes have moved a tad lower since its issuance as can be seen in the table below:

ABN AMRO raised €1.75bn via a two-tranche deal. It raised €1bn via a 3.5Y senior preferred bond at a yield of 3.958%, 20bp inside initial guidance of MS+85bp area. The bonds have expected ratings of A1/A/A+ and received orders over €1.4bn, 1.4x issue size. The Dutch bank also raised €750mn via a 10.25NC5.25 Tier 2 bond at a yield of 5.561%, 30bp inside initial guidance of MS+275bp area. The Tier 2 notes have expected ratings of Baa2/BBB-/BBB+ and received orders over €1.5bn, 2x issue size. The new Tier 2 bonds offer a new issue premium of 4.1bp over its existing 5.125% Tier 2 2033s, callable in 2027, that yield 5.52%. Proceeds will be used for general corporate purposes.

Health & Happiness International raised $200mn via a 3NC2 bond at a yield of 14.774%. The bonds have expected ratings of Ba3/BB+. Proceeds will be used to repay the company’s existing notes, including the tender offer for its 5.625% 2024s. Any remaining net proceeds are expected to be used to partially repay outstanding indebtedness under the senior facilities.

New Bonds Pipeline

- SK Broadband hires for $ 3Y or 5Y bond

- Pertamina Geothermal hires for bond

Rating Changes

- Fitch Upgrades Argentina’s FC IDR to ‘CC’; Affirms LC IDR at ‘CCC-‘

- Moody’s upgrades Chesapeake Energy’s CFR to Ba1

- Argentina Long-Term Local Currency Rating Raised To ‘CCC-‘ As Default Is Cured; ‘CCC-‘ Foreign Currency Rating Affirmed

- Fitch Revises Vodafone Group Plc’s Outlook to Positive; Affirms IDR at ‘BBB’

- Fitch Revises Outlook on Longfor to Stable; Affirms at ‘BBB’

ICYMI: We Are Merging Our Brands BondEvalue and BondbloX

We are excited to share that we will be merging our two brands – BondEvalue, our bond information service, with BondbloX, our award-winning bond exchange. BondbloX will be the name of the combined brand going forward. Read more about the change and what it means for you here.

Term of the Day

Equity Risk Premium

Equity risk premium refers to the extra expected return/spread that investors can get for holding stocks over the benchmark risk-free government bond. A higher premium indicates a greater compensation for risk that investors will bear for holding stocks vs. bonds. A lower premium would indicate the opposite.

Schroders, in an analysis of risk premiums noted that US equity investors today are “being rewarded with a smaller return premium for bearing equity risk than at any time in recent memory… More risk, less reward.”

Talking Heads

On Zambia’s Debt Restructuring Deal

Abebe Aemro Selassie, director of the African Department at IMF

“We’ve had initial agreements to provide financing assurances so the IMF can proceed with providing financing with Zambia.”

Situmbeko Musokotwane, Finance Minister of Zambia

“(IMF and Zambia are having) very very active discussions and we are very hopeful that something will come through in the next few weeks.”

Lu Ting, chief China economist at Nomura

“The room for traditional stimulus tools is increasingly small, and they have led to lingering negative impact in the past…(China’s high debt ratio means) it will be more difficult to roll out a support policy package… Cutting interest rates alone won’t be enough.”

Duncan Wrigley, chief China economist at Pantheon Macroeconomics

“The aim of stimulus this time is to keep growth ticking over…rather than to spur a round of robust growth…Policymakers are still wary of repeating the kind of debt hangover that the Global Financial Crisis stimulus produced and they spent the decade up to the pandemic trying to sort out.”

Larry Hu, head of China economics at Macquarie

“Policy is the only game changer (in the face of weak consumer and business confidence in the economy)…The rate cut today sent a clear signal that policy would turn more supportive in the coming months, a significant shift from the tapering in stimulus since April.”

On US Inflation and Fed Interest Rate Decision

Jamie Cox, managing partner at Harris Financial Group

“This CPI report is everything the Fed needs to pause — there is deflation and/or disinflation in every category…If this trajectory holds in June, the need for further tightening is behind us.”

Sarah House and Michael Pugliese, economists at Wells Fargo

“We expect a more pronounced slowdown in core inflation in the coming months…That said, directional progress should not be confused with mission accomplished.”

Ian Shepherdson, chief economics at Pantheon Macroeconomics

“Such rapid headline disinflation will make it harder for the Fed to justify raising rates again, but we can’t rule out a July hike yet.”

On How Stocks Stole Year of the Bond – co-CIO for global balanced risk at Morgan Stanley Jim Caron

“This is supposed to be the year for fixed income…the Federal Reserve and other central banks are increasing interest rates fast enough to reduce inflation, just not enough to meet the targets they’ve set…Which means their policy by definition relative to their own inflation target is going to run a little easier and that is going to be supportive for riskier assets…Bond yields have to stay likely lower than the Fed funds rate for an extended period of time. That in and of itself eases financial conditions because it puts more emphasis on riskier assets like equities and even high-yield credit.”

Top Gainers & Losers – 14-June-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.