This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Treasury Yields Spike Higher; Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

April 28, 2023

US Treasury yields shot higher across the curve following the economic data release yesterday that showed Core PCE rise alongside a fall in applications for unemployment benefits. The US 2Y Treasury yield is now back above 4%-mark at 4.08%, higher by 15bp. The 10Y yield was up 9bp to 3.53%. The US economy showed signs of a slowdown as GDP in Q1 rose by an annualized 1.1%, notably less than the median forecast for 1.9% and last quarter’s 2.6%. However, Core PCE during the quarter picked up to 4.9%, above last quarter’s 4.4% and also estimates of 4.7%. Also, initial jobless claims for the prior week witnessed a fall for the first time in three weeks, from 245k to 230k. US equity indices rose sharply as the S&P and the Nasdaq rallied by 2% and 2.4% respectively.

The Peak Fed funds was up 5bp to 5.11% for the June meeting. The uptick in yields also saw CME probabilities continuing to indicate a 25bp hike in upcoming Fed’s May meeting, with an 84% probability vs. 73% yesterday. US IG and HY CDS spreads were tighter by 2.9bp and 12.6bp respectively.

European equity markets ended higher too. European main CDS spreads were tighter by 1.8bp and Crossover spreads tightened 11.6bp. Asia ex-Japan CDS spreads tightened by 4.7bp. Asian equity markets have opened in the green today.

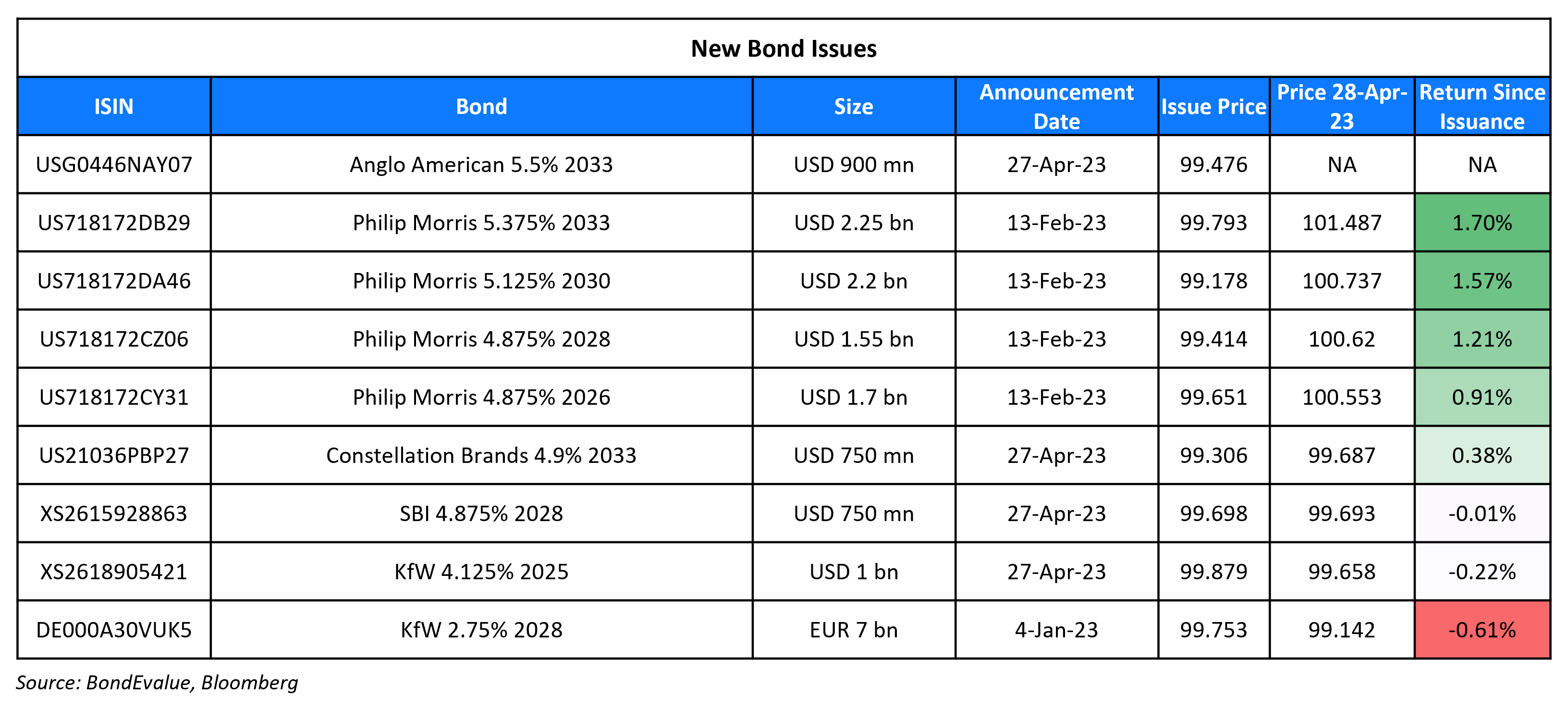

New Bond Issues

SBI raised $750mn via a 5Y bond at a yield of 4.944%, 40bp inside initial guidance of T+185bp area. The bonds have expected ratings of BBB-/BBB-, and received orders over $2.9bn, 3.9x issue size. As per IFR, a banker on the deal mentioned that “markets are constructive and there has been a lack of supply from India, both factors which have helped with demand.” Ultimately, asset and fund managers bought 43%, banks 40%, private banks and securities 5%, with other financial institutions making up the remaining 12%. Proceeds will be used for general corporate purposes in accordance with applicable law and to meet the funding requirement of the SBI’s foreign offices. The bonds have a put option at 101 if the total direct/indirect stake of the Government of India falls below 51%.

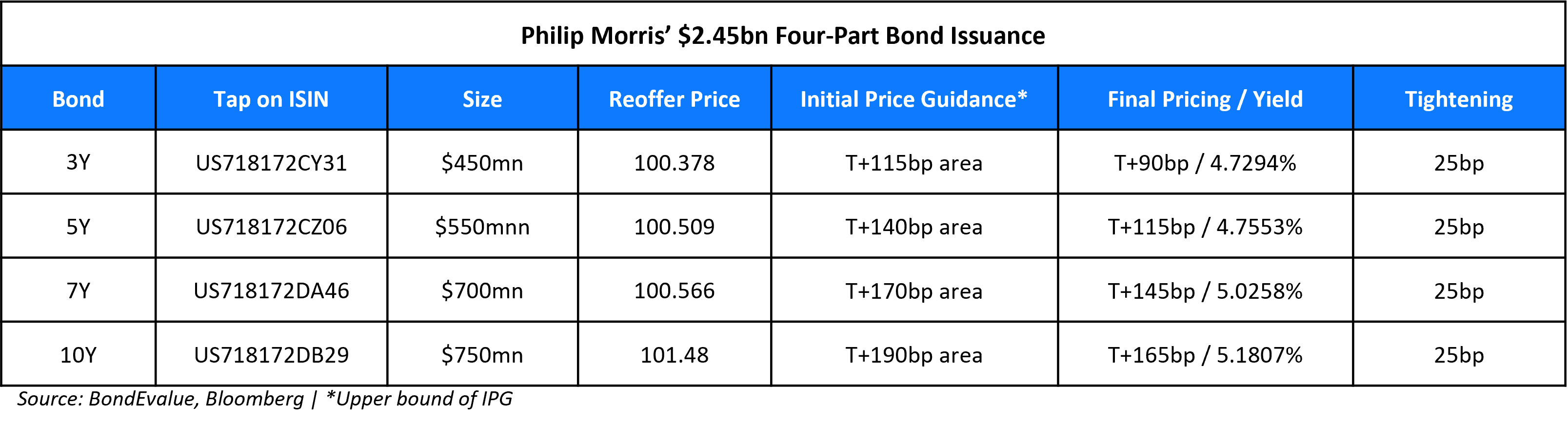

Philip Morris raised $2.45bn in a 4-tranche deal. The details are as follows:

The bonds have expected ratings of A2/A-/A. Proceeds will be used for general corporate purposes including repaying outstanding commercial paper, meeting working capital requirements, and paying a portion of or all the remaining cash consideration due in accordance with the terms of the Altria Agreement, regarding IQOS commercialization rights in the United States.

New Bonds Pipeline

- Banco BTG hires for $ bond

Rating Changes

- Mashreqbank Upgraded To ‘A’ On Higher Government Support; Outlook Stable

- Dish Network Corp. Rating Lowered To ‘CCC+’ On Cash Flow Uncertainty; Outlook Negative

- Air Canada Outlook Revised To Positive From Stable On Strong Passenger Demand

Term of the Day

Debt-For-Nature Swap

Debt-for-nature swaps are a transaction wherein an amount of debt owed by a developing country government is cancelled or reduced by a creditor, and swapped with a financial commitment earmarked for environmental conservation. Once the creditor reduces or cancels the debt repayment amount, both the creditor and debtor arrive at an agreed amount that would have otherwise been used for servicing the debt, to be used for environmental projects. These swaps typically involve countries that are distressed and find it difficult to repay offshore debt. The earnings generated through swaps are often administered by local conservation or environmental trust funds.

The world’s first debt-for-nature swap was between Bolivia and foreign creditors, who forgave $650k of its debt in exchange for setting aside 3.7mn acres of land adjacent to the Amazon Basin for conservation. Yesterday, Ecuador’s dollar bonds saw a spike higher after news about a debt-for-nature swap aimed at protecting the Galapagos Islands. For more details, click here

Talking Heads

On ‘Violent’ Emerging-Market Rout Coming – World’s biggest publicly listed hedge fund, Man Group

“Our argument is still pretty much in play. We have one of the most defensive positions we have ever had”… temporary rallies earlier this year were simply a consequence of dollar-liquidity dynamics.

Olga Yangol, head of emerging market strategy for Credit Agricole

“The rally in the markets over the past few months is largely driven by liquidity conditions. We expect the resolution of the debt ceiling impasse, the onset of the cyclical credit crunch, as well as potentially higher-for-longer Fed funds rate in the context of inflation persistence to send this into reverse…. we are underweight EM FX risk vs the dollar in our EM FX portfolio.”

On US debt ceiling technical default seen at 2%-3% – Fmr US Treasury Secy, Larry Summers

“I think the odds on a technical default associated with the debt limit legislation over the next few months are 2% or 3%, and if it happens it will be repaired fairly quickly… odds that we will default in the sense of insolvency, and over some interval people who hold bonds will not be able to get paid, are – assuming the absence of a major war – certainly under 2% over the next decade”

On One-Day VIX Showing Market’s Receding Fear of Inflation Data, Fed Decisions

Danny Kirsch, head of options at Piper Sandler & Co.

“There seems like less uncertainty on what the Fed will do. It’s much closer to the end of hiking. Options have been too expensive past several FOMC and CPI so the market was discounting perhaps too much”

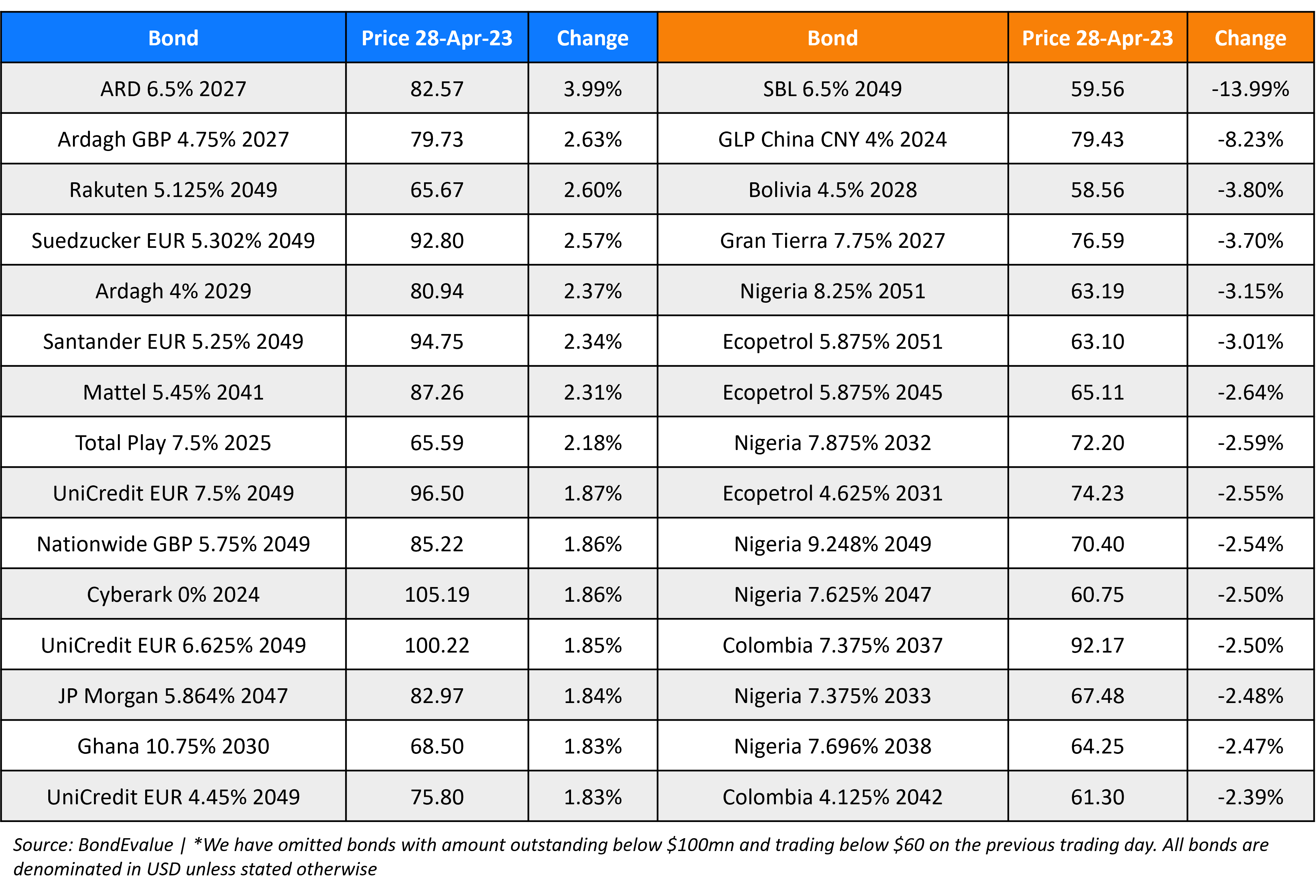

Top Gainers & Losers – 27-April-23*

Other News

Evergrande extends deadline for debt restructuring incentive to May 18

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.