This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

US CPI and Core CPI Come In-Line With Estimates

December 13, 2023

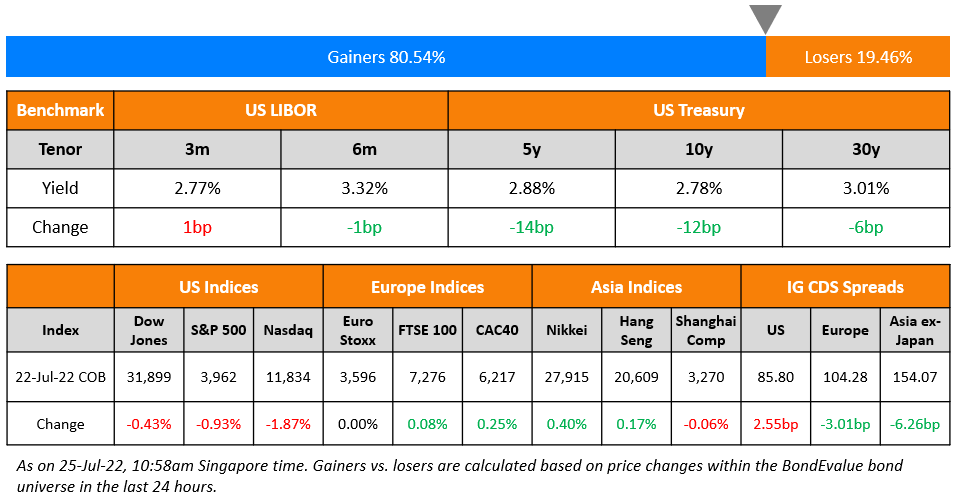

US Treasury yields were broadly stable across the curve after the inflation report was broadly inline with expectations. US CPI for November 2023 came at 3.1%, inline with expectations of 3.1% and lower than previous month’s 3.2%. Core CPI was at 4.0%, inline with expectations and the prior month’s 4.0% print. All eyes now turn towards the FOMC meeting later today for takeaways on the forward guidance of rates, as the Fed is expected to keep rates steady. US credit markets saw IG CDS spreads tighten by 1.6bp and HY by 8bp. US equity markets ended higher with the S&P and Nasdaq up 0.5-0.7% respectively.

European equity markets ended flat. In credit markets, European main CDS spreads were 0.4bp tighter while crossover spreads widened by 4.3bp. Asian equity markets have opened weaker today. Asia ex-Japan IG CDS spreads were tighter by 1.1bp.

One-day course on bonds in Singapore | 14 Dec | 50/70% Funding for Locals

.png)

New Bond Issues.png)

New Issues Pipeline

- India Vehicle Finance hires for $ 6.5Y Sr Secured bond

Rating Changes

- Fitch Upgrades Rolls-Royce to ‘BB+’; Outlook Positive

- Moody’s downgrades Braskem’s ratings to Ba2; changes outlook to negative

- Sibanye Stillwater Ltd. Downgraded To ‘BB-‘ On Low Commodity Prices And Debt Increase; Outlook Negative

Term of the Day

Widow-Maker Trade

A widow-maker trade is considered to be a particular trade that repeatedly surprises markets and defies historical patterns, thereby resulting in large losses. These trades are typically considered rational and sometimes even the most obvious as patterns like mean-reversion or consensus views may seem the most likely outcome. However, the actual market moves

One of the most popular widow-maker trades spoken about is that of shorting Japanese government bonds (JGBs). Several traders have shorted JGBs over the past decades given the massive rise in Japanese government debt, very loose monetary policy and expectations of a eventual pick-up in inflation. As with widow-maker trades, this trade would logically seem to make sense. However, the BOJ has only pushed interest rates lower and continued to keep policy broadly loose. Thus, JGB prices have moved higher and made “widows” of many traders.

Some analysts have again made calls for shorting JGBs in 2024 noting that it may work as rising inflation may put pressure on the BOJ to adopt a tighter policy. This is in addition to BOJ’s already relaxed yield-curve-control policy this year.

Talking Heads

On Weakened EU Needing Bold Plan to Exit Crises – ECB’s Villeroy

“The dangerous world of 2023 requires the reawakening of Europe, a force for peace and cooperation. And the anxious Europeans of 2023 need the reawakening of Europe, if we are to fulfill our promise of a sustainable prosperity… euro-area inflation has slowed to 2.4%, down from its October 2022 peak of 10.6%. “The path between these two figures is impressive”.

On Bond Forecasters of 2023 Saying Rally Likely to Fizzle

Praveen Korapaty, chief interest-rate strategist at Goldman Sachs

“Markets are pricing too much policy easing too soon”… predict that the 10-year Treasury yield will climb to about 4.5% by the end of next year… slightly bigger risk that yields may rise above his base-line scenario of 4.55% if inflation prove sticky.

BMO Capital Markets’ Scott Anderson

See Treasuries almost unchanged from current 4.2%… “Our longer-term forecast on the Fed over the next five years is that the Fed funds rate won’t be moving back down to pre-pandemic levels anytime soon”

On Top Trading Ideas for Asia in 2024 by Big Money Managers

Wylie Tollette, CIO at Franklin Templeton Investment Solutions

“We think Asia might be well positioned for the return of positive bond returns — and the return of the negative correlation tailwind”

Zijian Yang, head of multi-asset APAC at Allianz Global Investors

“The yen’s extremely cheap valuation has sustained for so long — we believe there ought to be a turning point”

Seema Shah, chief global strategist at Principal Asset Management

“The key plus-point for India is the fundamental outlook for growth… lot of investor optimism and confidence now”

RBC Wealth Management analysts Kennard Ling and Shawn Sim

“Asia high-yield is out of favor, and we view the asset class as less attractive amidst macro uncertainties and concerns regarding idiosyncratic risks”

Top Gainers & Losers- 13-December-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.