This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

US CPI at 3.7%; Core CPI at 4.3%

September 14, 2023

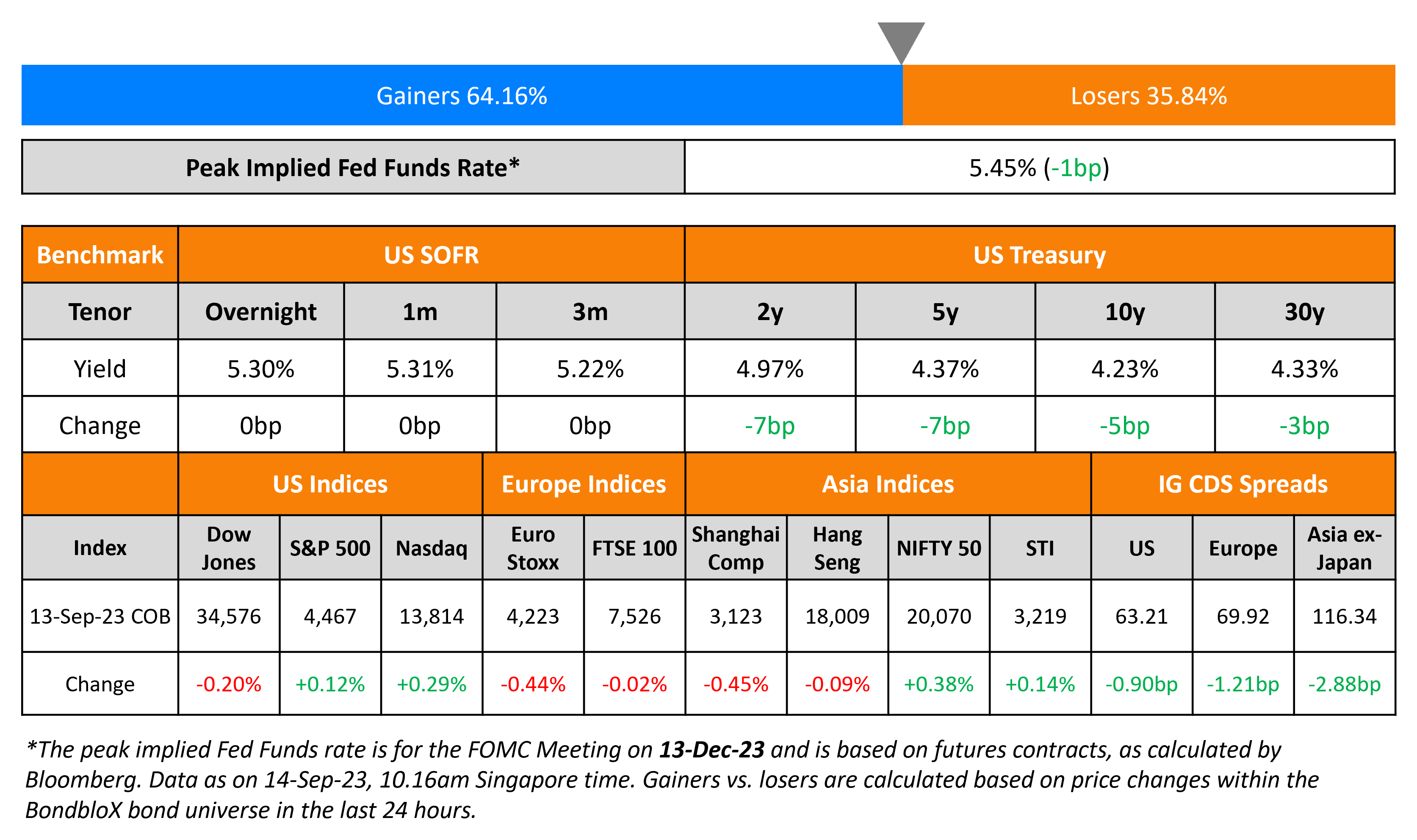

US Treasury yields moved lower across the curve by 5-7bp following the US inflation report. US CPI for August 2023 came at 3.7%, higher than expectations of 3.6% and the previous month’s 3.2%. Core CPI continued its downward trend to 4.3%, inline with expectations of 4.3% and lower than the previous month’s 4.7%. JPMorgan Asset Management has come out saying that it expects the Fed not to hike rates any further in the current cycle. The probability of a 25bp rate hike at the November meeting did not change much following the CPI report, remaining at 40%. IG CDS spreads were 0.9bp tighter while HY spreads tightened by 3.9bp. The S&P and Nasdaq moved higher by 0.1% and 0.3% respectively.

European equity markets ended slightly lower. In credit markets, European main CDS spreads were tighter by 1.2bp with crossover spreads tightening 5.4bp. Asian equity markets have opened broadly mixed this morning while Asia ex-Japan CDS spreads tightened 2.9bp yesterday.

New Bond Issues

- Bangkok Bank $ 5Y/10Y at T+135/165bp area

- Korea Southern Power $ 3Y at T+130bp area

Sharjah raised $750mn via a 10.5Y sukuk at a yield of 6.092%, 40bp inside initial guidance of T+220bp area. The senior unsecured bonds are unrated but the issuer is rated Ba1/BBB- (Moody’s/S&P). The deal received orders over $3.4bn, 4.5x issue size. The new bond is priced ~25bp tighter to its existing 3.625% bonds due March 2033 that yield 6.34%.

New Bond Pipeline

- Arcelik hires for $ 5Y bond

- Energy Development Oman hires for $ 10Y sukuk

- Emirates NBD hires for Sustainable bond

- FWD hires for $ 10Y bond

Rating Changes

- Jamaica Long-Term Ratings Raised To ‘BB-‘ From ‘B+’ On Improved Finances; Outlook Stable

- Fitch Downgrades VF Ukraine to ‘CCC-‘

Term of the Day

Treasury Basis Trade

The Treasury Basis Trade is a trade which involves buying/selling a treasury bond and simultaneously taking the opposite position in a corresponding treasury futures contract. When a trader buys the bond and sells the futures, it is considered to be a ‘long basis’ trade and when he/she sells the bond and buys the futures, it is a ‘short basis’ trade. Fed economists reported that the cash-futures basis positions could be exposed again to stress during broader market corrections. The unwinding of basis trades contributed to illiquidity in Treasuries in March 2020 and Fed economists want to prevent another event of a similar origin.

Talking Heads

On Bonds Stymied as Inflation Data Fails to Break Fed-Hike Logjam

Gang Hu, managing partner at Winshore Capital Partners

“The inflation theme is still around. So we move on. The key these days is oil”

Michael Pond, head of global inflation-linked research at Barclays

Upside surprise in core inflation was largely driven by airfare, which “is unlikely to change views about to path of inflation”. Short term TIPS relative to regular Treasuries, “offer the best value to trade upside inflation risk.”

On Fed economists sounding alarm on hedge funds gaming US Treasuries

Fed Economists

“Cash-futures basis positions could again be exposed to stress during broader market corrections. With these risks in mind, the trade warrants continued and diligent monitoring.”

Steven Zeng, US rates strategist at Deutsche Bank

“The Fed is unlikely to view this accumulation of basis positions under too favorable a light and may eventually want to clamp down on them. However, the approach they take may not be straightforward as the Fed does not have direct regulatory oversight over hedge funds”

On EMs Boosted by Interventions as Rate Fears Grow

Marek Drimal, a London-based strategist at SocGen

“Risks that the Fed and the ECB will remain hawkish for longer have put sentiment in emerging markets on the back foot. In addition, inflation pressures in several EM countries continue to be elevated”

On Warning of Soft Landing Chances Only 1-in-3: Former US Treasury Secy, Larry Summers

“It’s a very narrow window to achieve that soft landing… the Fed is right to be data dependent”… “There is no sign” at this point that this is a “2% inflation economy”… about a one-in-three chance for each of three scenarios: a soft landing, a “no landing, with inflation never really getting below 3%,” and a harder landing where the Fed’s cumulative rate hikes hit the economy.

Top Gainers & Losers- 14-September-23*

Other News

China to issue yuan bonds in Macau, targeting financial services in bid to diversify its economy

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.