This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

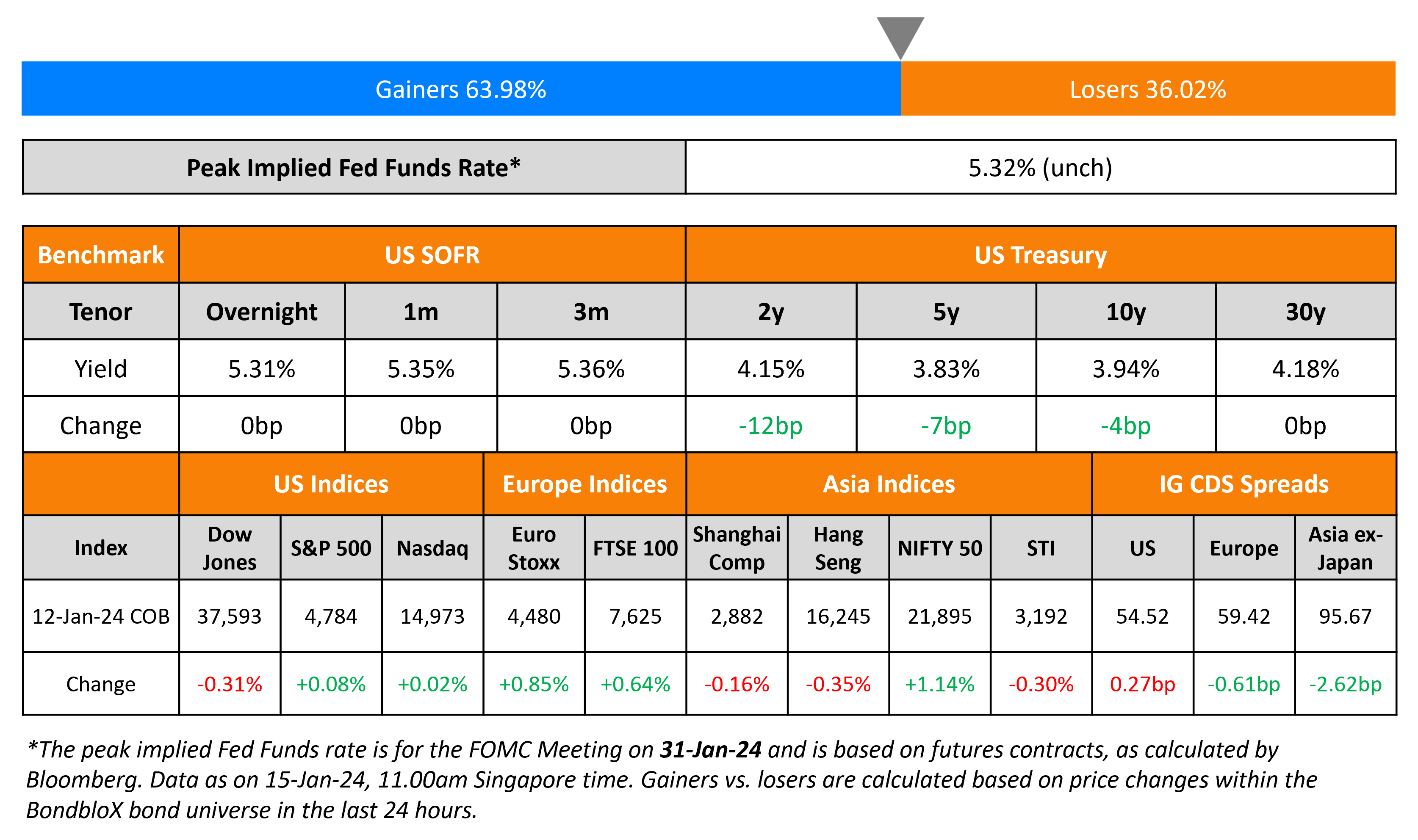

US IG CDS Spreads at 2Y Lows; Yields Drop After Soft PPI

January 15, 2024

US Treasury yields dropped across the curve on Friday, with the front-end being impacted the most. The 2Y yield fell 12bp to 4.15% while the 10Y fell 4bp to 3.94%. US producer prices, as measured by the Producer Price Index (PPI) fell 0.1% MoM in December vs estimates of a 0.1% pick-up. On a YoY basis, it rose by 1% vs expectations of a 1.3% rise. Goods prices dropped 0.4%, going into deflation territory. Separately, oil prices have risen following the situation at the Red Sea. Brent crude touched $80/bbl and is currently at over $77.5/bbl. Looking at credit markets, US IG CDS spreads widened by 0.3bp and HY spreads widened 1.9bp. US equity markets traded broadly flat, with the S&P and Nasdaq ending almost unchanged on Friday.

European equity markets ended higher. Credit markets in the region saw the European main CDS spreads tighten by 0.6bp and crossover spreads tighten by 3.6bp. Asian equity markets have broadly opened in the green today. Asia ex-Japan IG CDS spreads tightened by 2.6bp.

New Bond Issues

.png)

New Bond Pipeline

- Shriram Finance hires for $ Social bond

- Sumitomo Mitsui Finance hires for $ 5Y bond

- SATS hires for $/S$ 5Y bond

- Greenko Plans for up to $450mn bonds

- SK Battery America 3Y Green bond

Rating Changes

- Moody’s changes outlook on Turkiye to positive, affirms B3 ratings

- DISH DBS Corp. Debt Ratings Lowered On Asset Transfers

- Vedanta Resources Downgraded To ‘SD’ On Completion Of Liability Management Transaction

- Fitch Revises Embraer’s Outlook to Positive; Affirms IDR at ‘BB+’

Term of the Day

Credit Default Swap (CDS)

A Credit Default Swap (CDS) is a financial contract between two counterparties that allows an investor to “swap” or offset the credit risk with another investor. CDS acts like an insurance policy wherein the buyer makes regular payments to the seller to protect itself from an issuer default. In the event of a default, the buyer receives a payout, typically the face value of the bond or loan, from the seller of the CDS as per the agreement. CDS spreads are a commonly used metric to track the market-priced creditworthiness of an issuer. A widening (increase) in CDS spreads indicates a deterioration in creditworthiness and vice-versa.

Talking Heads

On Argentina, Turkey Lure Investors Seeking High-Yield Bond Returns

David Robbins, debt fund at TCW

“We have overweights across the high-yield space in a select group of countries — and we believe in those fiscal consolidation stories… you probably won’t see any defaults in the sovereign space”

PMs at at Vontobel Asset Management

“With lower US Treasury yields, many high-yield issuers are likely to regain market access over the next 12 months… a virtuous cycle as the fear of default is taken off the table”

Eamon Aghdasi, EM analyst at Grantham Mayo Van Otterloo & Co

“The balance of risk is still positive in that country. You could, if things work out, see a continued nice performance in Argentina. We’re still overweight”

On More Stocks and Bonds Are Moving In Tandem, Worrying Some on Wall Street

Andrew Lapthorne, SocGen’s head of quantitative research

“Without bond yields going down a large chunk of the market has a significant valuation headwind. We have a lot of market capitalization that is expensive, and this is creating a positive correlation to bonds”

Michael Purves, the founder of Tallbacken Capital Advisors

“CPI report demonstrates that while inflation is broadly in retreat, the pace of that retreat is slowing. The bar for cuts is simply a lot higher”

On US 20Y Bond ‘Comeback’ Merits More Supply – Deutsche Bank

“Should win the comeback player of the year award if there was one for bonds… saw a resurgence in popularity last year

On Higher-for-Longer Yields Being the Star Attraction in Bond Deluge

Del Canto, co-head of capital markets for EMEA at MUFJ

“Conditions are incredibly strong right now and executions are largely meeting a very receptive audience. After last year’s volatility, issuers know that such a reception is all but guaranteed”

Matt Brill, head of North America IG at Invesco Advisers

“If you can lock in and be guaranteed by a high-quality corporation that you’re going to be getting the coupon for the next 30 years”

Top Gainers & Losers- 15-January-24*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.