This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Average US IG Yields at Highest Since 2009

October 4, 2023

US Treasuries extended their sell-off on Tuesday as yields soared on the long-end. The 10Y and 30Y yields were up over 14-16bp while the 2Y was up 4bp as the curve bear steepened. US JOLTS Job Openings jumped to 9.6mn in August, much higher than forecasts of 8.8mn continuing to imply a resilient economy and further strengthening the ‘higher for longer’ theme. Separately, the average yield on US investment grade bonds have now hit 6.27%, the highest since 2009 (as seen in the chart below). Meanwhile, the average yield on US high yield bonds have touched 9% for the first time since June, with credit spreads hovering at ~400bp over treasuries. In credit markets, US IG CDS spreads were 3.3bp wider while HY spreads widened 20bp. US equities dropped with the S&P and Nasdaq down 1.4% and 1.9% respectively.

European equity markets ended lower again. In credit markets, European main CDS spreads were wider by 3.7bp and crossover spreads widened 16bp. Asian equity markets have opened lower this morning, down over 0.5%. Asia ex-Japan IG CDS spreads have widened another 3.5bp.

New Bond Issues

Emirates NBD raised $750mn via a 5Y Green bond at a yield of 5.903%, 20bp inside initial guidance of T+140bp area. The senior unsecured bonds have expected ratings of A2/A+ (Moody’s/Fitch), and received orders over $1.9bn, 2.5x issue size. Proceeds will be used to finance/refinance new or existing eligible assets in accordance with the issuer’s sustainable finance framework.

New Bond Pipeline

- Damac Real Estate hires for $ 3.5Y sukuk bond

- Oman Telecom hires for $ 7Y sukuk bond

- Uzbekistan hires for $ 5Y/10Y bond

- Philippines hires for $1bn Retail bond

Rating Changes

- Fitch Downgrades PERU LNG to ‘B’; Assigns Negative Outlook

- Fitch Downgrades Unigel’s IDRs to ‘C’

- Fitch Revises Boeing’s Outlook to Positive; Affirms IDR at ‘BBB-‘

Term of the Day

Yield To Worst

Yield to worst (YTW) is a useful metric to track and compare bonds that have a call option. For non-callable bonds, there is a single measure of yield i.e. yield to maturity (YTM). Callable bonds have an additional measure of yield called yield to call (YTC), which calculates the bond’s yield with the assumption that the bond will be called on the bond’s call date. YTW is the lower of YTM and YTC, making it the conservative measure of yield.

Talking Heads

On Bond Rout Deepens With No Peak in Sight for Rates

Michael Cloherty, head of US rates strategy at UBS Securities

“The speed of the move has scared all the value buyers. If you can hold a trade for three months, you’re happy. It’s what happens in the next 72 hours that’s the trouble here”

John Brady, MD at RJ O’Brien

“Real yields on the long end just have further to go…. pace of inflation falling is not satisfactory enough…Fed’s framework for getting inflation lower is to slow the economy, and that’s not exactly happening to the market’s satisfaction”

On State Street Betting Fed ‘Dramatically’ Cuts Rates Next Year – CIO, Lori Heinel

“Fed fund rate needs to drop pretty dramatically next year. We think at least four rate cuts — so 100 basis points and maybe as much as 200… We are buyers of rates here, there’s good value…. We’re going to see a slowing environment and central bankers are going to finally feel like they’ve done enough”.

On Credit Market Volatility as Fed Speak, Data

David Knutson, senior investment director at Schroder Investment

“The market is starting to price higher for longer”

Jack Parker, associate PM at Brandywine Global

“The market seems extremely skittish at the moment given rate volatility, hawkish Fed rhetoric and a hot JOLTS number… Headlines focused on elevated expected defaults might spook some investors, but there are plenty of high quality credits trading at historically high yields “

“All else being equal, this would be significantly bullish for Indian bond yields… additional source of financing for the current account and fiscal deficits through foreign inflows is positive for the currency and bond yields”

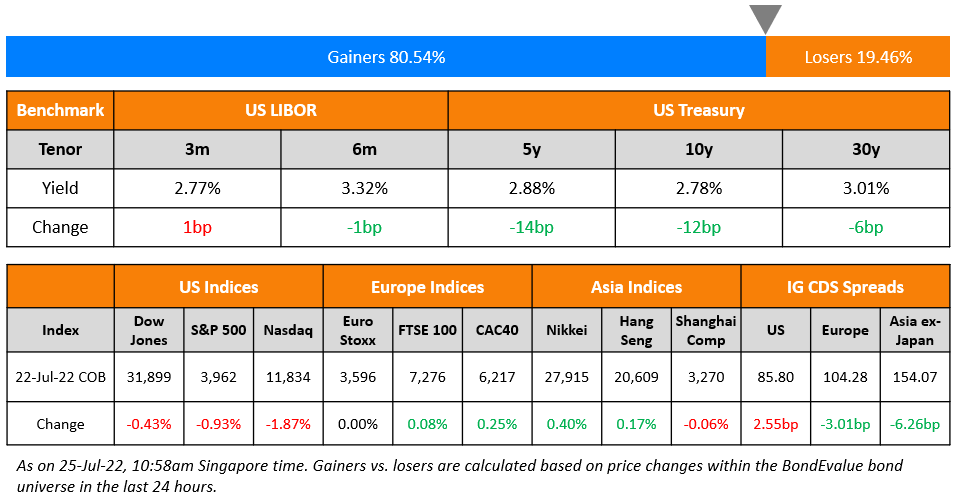

Top Gainers & Losers- 04-October-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.