This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

US Treasuries Extend Sell-Off

October 3, 2023

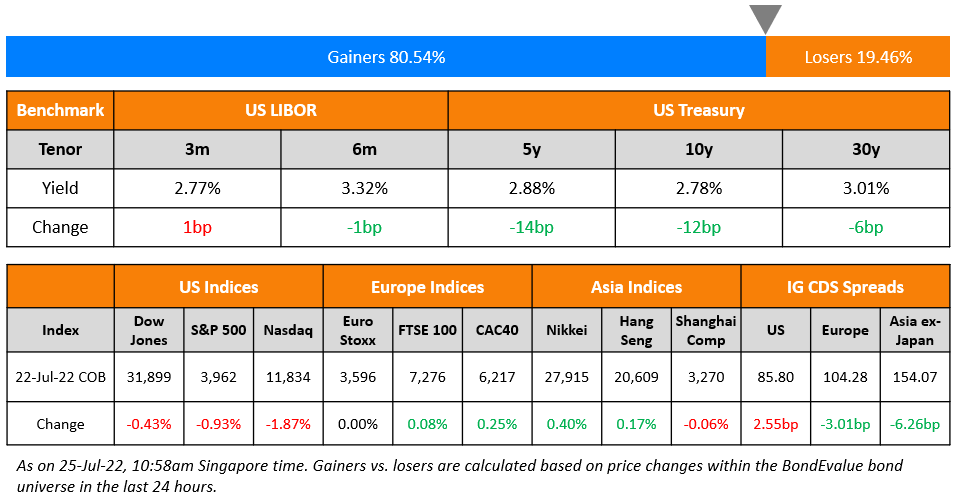

The sell-off in US Treasuries continued as yields jumped across the curve, led by the long-end. The 10Y yield was up over 6bp and the 2Y climbed 3bp higher. US ISM Manufacturing PMI increased to 49 in September from 47.6 a month prior, an eleventh straight month of contraction. However, the reading was just below the 50 mark that indicates ‘neither growth nor contraction’, thus showing an improvement. Analysts note that the soft landing narrative still remains thanks to the economy’s continued resilience on other fronts whilst the manufacturing sector appears to stage a minor recovery. The Prices Paid component fell to 43.8 vs forecasts of 49. However, the New Orders and Inventories components were better than expected and the Employment component went into expansion territory at 51.2. The peak fed funds rate was steady at 5.46%. In credit markets, US IG CDS spreads were 0.8bp wider while HY spreads widened 5.8bp. US equities were mixed with the S&P trading flat while Nasdaq was up 0.7%.

European equity markets ended lower. In credit markets, European main CDS spreads were wider by 2.9bp and crossover spreads widened 11.2bp. Asian equity markets have opened lower this morning, down over 0.5%. China’s equity market is closed due to the Golden Week holidays. Asia ex-Japan CDS spreads were 0.6bp wider.

New Bond Issues

New Bond Pipeline

- Damac Real Estate hires for $ 3.5Y sukuk bond

- Oman Telecom hires for $ 7Y sukuk bond

- Uzbekistan hires for $ 5Y/10Y bond

- Philippines hires for $1bn Retail bond

- Emirates NBD hires for Sustainable bond

Rating Changes

- Fitch Upgrades TUI Cruises’ IDR to ‘B’; Outlook Positive

- Moody’s downgrades Magellan notes to Baa2, outlook stable

- Fitch Revises Panama’s Outlook to Negative, Affirms IDR at ‘BBB-‘

Term of the Day

PMI

PMIs or Purchasing Managers’ Index are an index composed of a monthly survey of purchasing managers/supply chain managers across industries. This is a diffusion index, a statistical measure of summarizing the common tendency of a series – if there are more number of values rising than falling, the index is above 50 and the index goes below 50 if the falling values exceed those rising. For PMIs, a value below 50 indicates contraction and a value above 50 shows expansion. These surveys are taken over different areas of the supply chain business: New Orders, Employment, Inventories, Supplier Deliveries and Production covering imports, exports, prices and backlogs. In most countries, Markit publishes the PMI numbers while other organizations publish them too. Markit generally publishes the month’s PMIs in last week of the month. In the US, the Institute of Supply Management (ISM) publishes the official PMIs during the first week of the month.

Talking Heads

On BOJ Fighting Back Key to Stopping Treasuries Selloff

Adrian Janschek, PM at First Sentier Investors

Investors want to “watch the Bank of Japan back the truck up and go: ‘it’s not going past 1%, we told you this. Everyone goes, okay, we’re up 4.70%, 4.80% in the US 10-year, let’s get in. I think that’s what needs to happen before people get really comfortable.”

Naoya Hasegawa, senior bond strategist at Okasan Securities

“Long-term and super-long yields have faced upward pressure basically due to concerns about the BOJ’s potential tweak”

On US bond market signaling the end of an era

Greg Whiteley, PM at DoubleLine Capital

“We have moved into a new era here. It’s not going to be a matter of struggling to get the inflation rate higher. It’s going to be working to keep it down”

Emanuel Moench, ACM Term Premium Fed model Author

“A very deep pocketed Treasury investor is leaving the market little by little. That should add to some uncertainty around the likely path of Treasuries”

John Velis, macro strategist for the Americas at BNY Mellon

“The r-star over the long-term is probably higher than the Fed thinks it is… disinflationary impulse of the post-GFC period is over”

On Morgan Stanley Now Bearish on Egypt

“In the near term, we think that Egypt lacks a positive catalyst, leaving us disliking the credit… long-term drag on the credit remains the high financing needs this year into next year, particularly at a time when market access remains uncertain for single-B credits like Egypt”

Top Gainers & Losers- 03-October-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.