This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

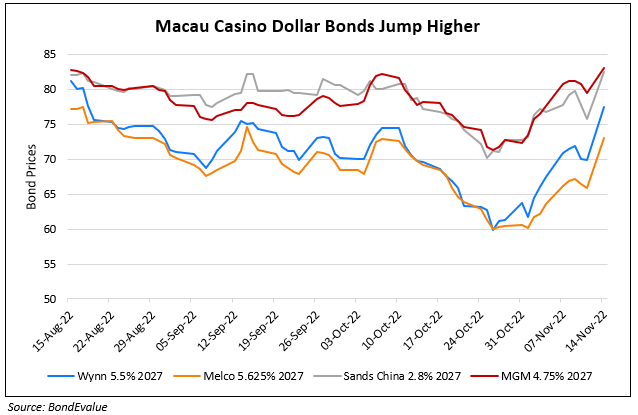

Bond Market News

Wynn Resorts, Macau Upgraded to BB- by S&P

November 16, 2023

Wynn Resorts and Wynn Macau were upgraded to BB- from B+ by S&P. The rating agency cites the recovery in the gaming mass market to support deleveraging and help reduce Wynn’s debt-to-EBITDA to low-5x by end-2023 and below 5x in 2024. Its gross gaming revenues (GGR) are forecasted to increase 20-30% YoY in 2024, led by the premium segment. Regarding the recovery following the pandemic, Wynn’s Macau GGR and reported EBITDA were about 97% and 85% of 2019 levels and are set to move higher in 2024. S&P believes that Wynn can absorb its planned development spending in Macao, Boston, and the UAE whilst still reducing leverage. Thanks to new 10-year concessions in December 2022 by the government, Wynn has committed to invest $2.2bn over this period.

Wynn’s dollar bonds were trading slightly higher with its 5.625% 2028s up 0.7 points to 87.8, yielding 8.8%.

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.