This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

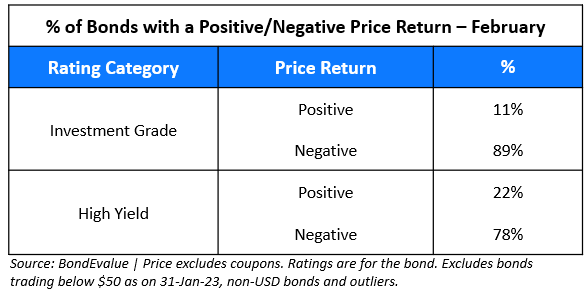

February 2023: Upside Surprise in Inflation Triggers Bond Market Sell-Off as 85% of Dollar Bonds End Lower

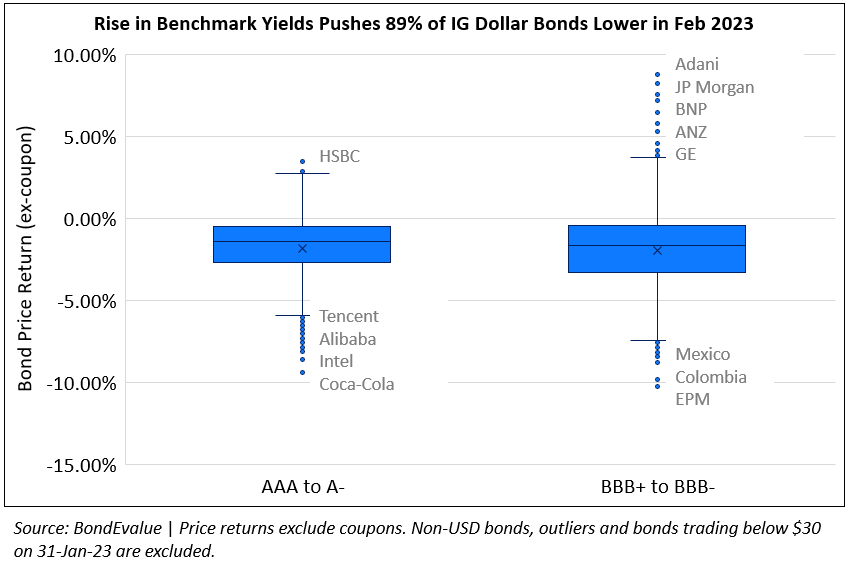

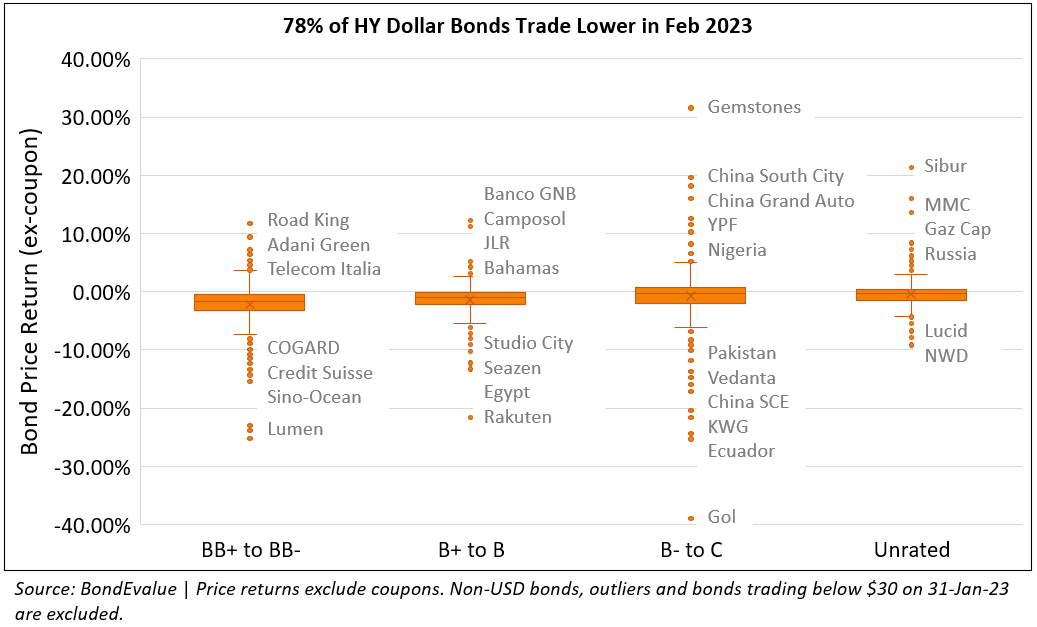

The month of February saw a reversal in fortunes for bond investors after a stellar performance in January, with 85% of the dollar bonds in our universe delivering a negative price return (ex-coupon). This was largely on the back of a sharp rise in benchmark yields last month after the higher-than-expected inflation print and strong jobs report in the US. The move higher in rates was led by the short-end where 2Y yields soared by 62bp while the 10Y yield jumped 41bp. 89% of all Investment Grade (IG) dollar bonds in our universe ended February in the red, underperforming the High Yield (HY) segment that saw 78% of dollar bonds in the red.

US Non-Farm Payrolls came at 517k for January, significantly beating the surveyed 189k. The keenly watched Average Hourly Earnings YoY rose to 4.4%, higher than the surveyed 4.3%, but lower than last month’s 4.6% print. Similarly, US CPI came at 6.4% for January, above expectations of 6.2% and lower than last month’s 6.5% print. Core CPI came at 5.6%, above the surveyed 5.5% and lower than last month’s 5.7% print. The Fed’s preferred inflation gauge, the Core PCE also came in higher than expected at 4.7% (vs. 4.3% est) at the end of the month. Thus, while some softening in inflation is being seen, the pace of deceleration was slower than what markets expected. On the back of this, some Fed speakers including Powell hinted at a higher peak Fed Funds rate and thereby, higher rates for longer. As a result, the peak Fed Funds rate has climbed up to 5.42% currently from 4.93% at the start of February. Looking forward, markets are pricing in a 25bp hike at each of the next three FOMC meetings.

The move higher across benchmark yields especially saw IG bonds underperform due to its greater duration sensitivity. Among the few gainers in the IG space were bonds of Adani Group that recovered during the month - this was led by Adani Green's 2024s after the company said that it will come up with a plan to refinance its bonds. In the latest update after conducting roadshows in Singapore and Hong Kong, Adani's CFO said that it was not seeking to refinance debt or inject capital. As per attendees of its roadshows, executives said that the Adani group has enough money to repay debt due over the next three years in addition to an $800mn credit facility. Separately, floating rate perpetual bonds of banks like BNP Paribas and ANZ with resets coming up; the bonds rose by 7-8% through the month, given their low sensitivity to rates. The losers list saw high duration/long tenor of highly rated corporates like Coca-Cola, Berkshire Hathaway, Alphabet, Alibaba, Dell, Oracle and others fall by over 7% during the month. LatAm sovereigns like Mexico and Colombia also saw their bonds down over 10%.

Issuance Volumes

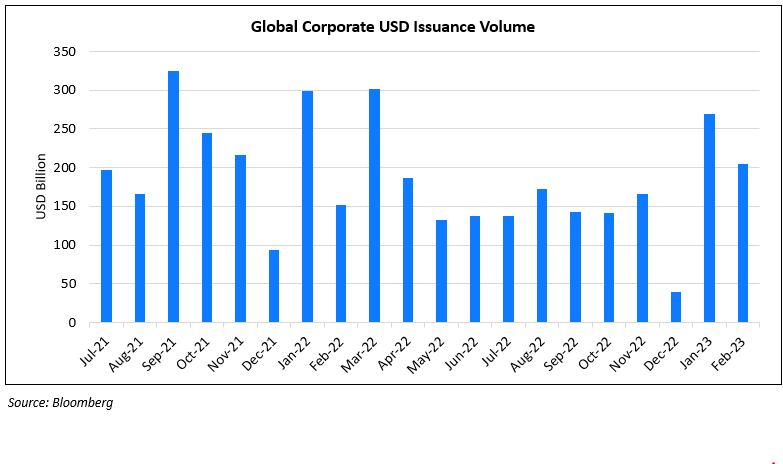

During the entire month, global corporate dollar bond issuances stood at $221.4bn vs. $269.9bn in January. lower by 18% MoM. As compared to February 2022, issuance volumes were over 46% higher YoY. 92% of the issuance volumes came from IG issuers with HY and unrated issuers taking the remainder. BofA strategists noted, "The heavy February volumes are likely driven by companies front-loading supply. That leaves a smaller borrowing need for March".

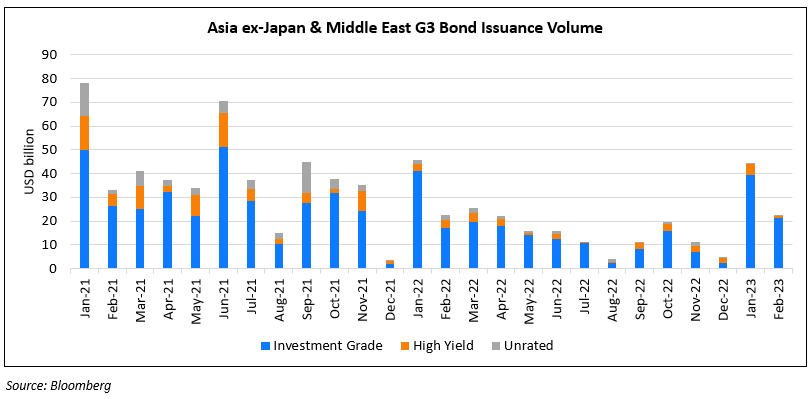

Investment Grade bonds' issuance volumes for the first two months of the year were at its highest on record (see chart below). As per Bloomberg, volumes are about a quarter of the entire $1.2tn that is expected by IG issuers in all of 2023 as per market analysts.

Investment Grade bonds' issuance volumes for the first two months of the year were at its highest on record (see chart below). As per Bloomberg, volumes are about a quarter of the entire $1.2tn that is expected by IG issuers in all of 2023 as per market analysts.

Asia ex-Japan & Middle East G3 issuances stood at $22.5bn, down 50% MoM and almost unchanged YoY. 96% of the volumes came from IG issuers while HY issuances were at a mere $680mn, down 85% MoM. As compared to January, IG issuances were 45% lower MoM.

Largest Deals

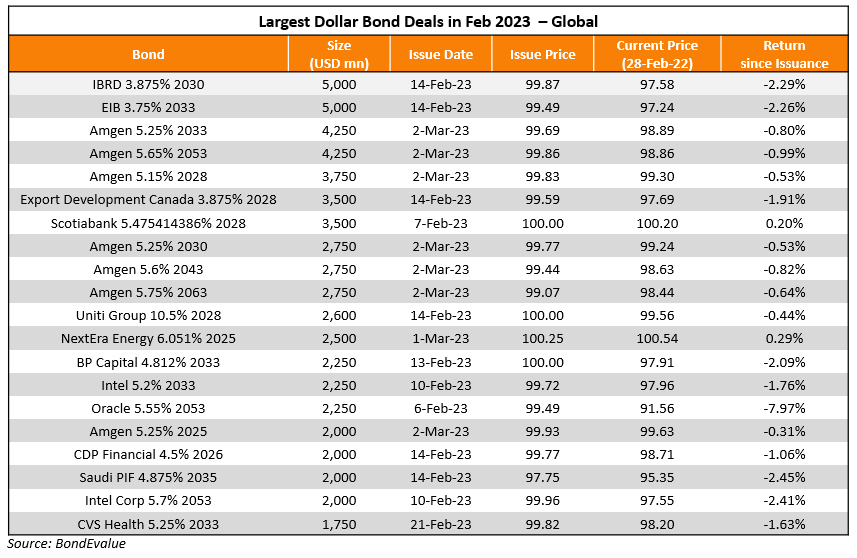

The largest deals in February 2023 was Amgen's jumbo $24bn eight-part deal, the biggest this year from an issuer, followed by Intel’s $11bn jumbo seven-part deal and CVS' $6bn four-trancher. Besides, Oracle's $5.25bn four-trancher, supras like IBRD and EIB's $5bn issuances each added to the sizeable deals.

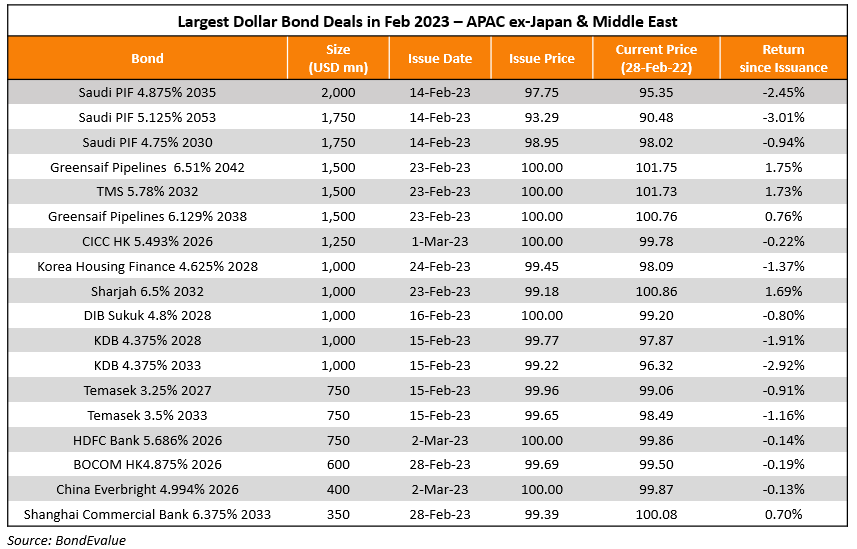

In the APAC & Middle East region, the largest deals was by the Saudi PIF that raised $5.5bn via a three-trancher, followed by Greensaif Pipelines that raised $3bn via a dual trancher. Other notable deals included KDB's $2bn dual-trancher, CICC HK's $1.25bn deal, Sharjah's $1bn issuance, and Temasek's $1.5bn deals. From India, HDFC Bank raised $750mn via a rare 3Y paper from the region.

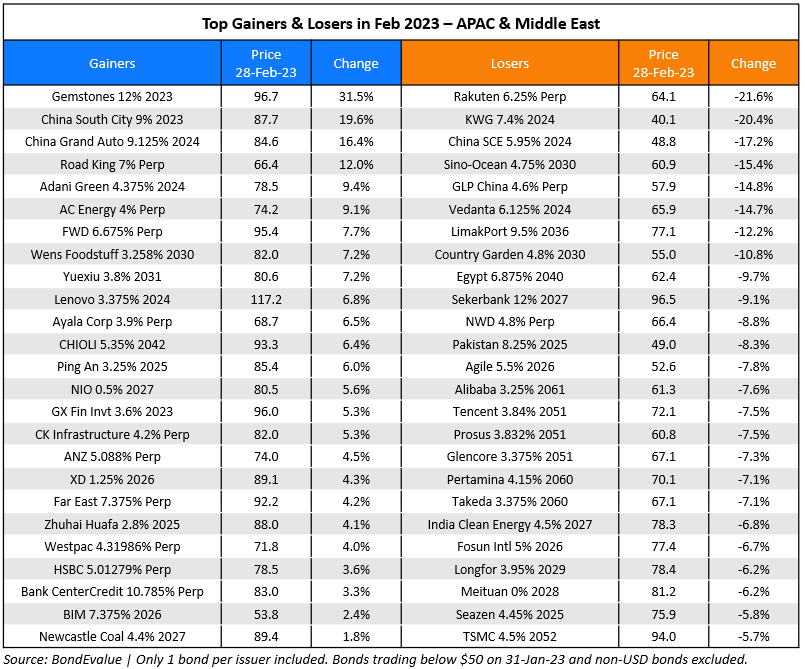

Top Gainers & Losers

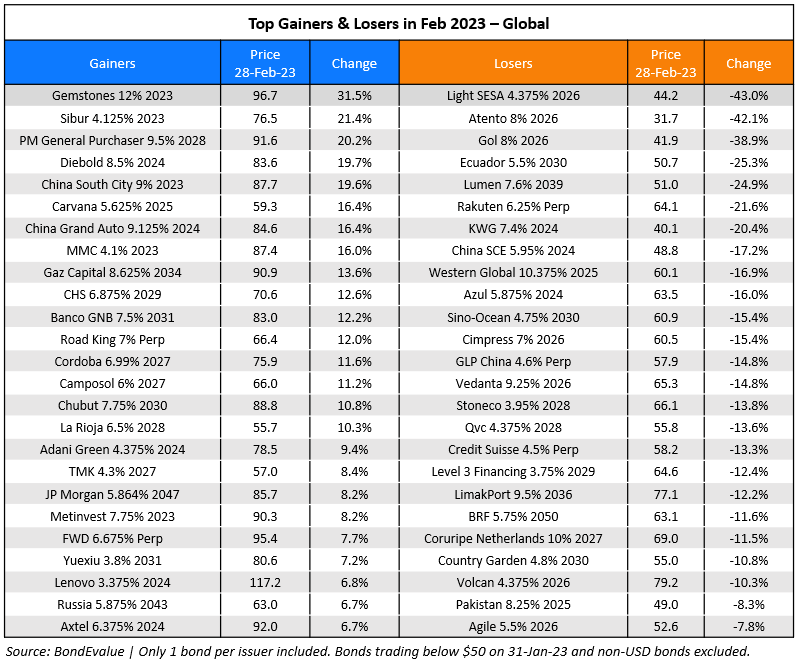

The biggest gainer during the month was Gemstones' 12% 2023s that jumped 26% after the company bought back $59.7mn of the notes with the bonds nearing its maturity date of March 10. China South City's dollar bonds also jumped over 20% after the Shenzhen government was said to have held a meeting to discuss facilitating a syndicated loan to China South City on the company’s Wechat account. Besides these companies, Russian companies like Sibur, Gazprom, TMK Group also rallied by over 8% during the month. Dollar bonds of Adani Group also recovered during the month, led by Adani Green's 2024s after it said that it will come up with a plan to refinance its bonds. Besides, the group also paid up on its other bonds' coupons without any signs of difficulty.

On the losers list, Brazilian high yield issuers like Light SESA, Atento and Gol dropped by over 33% amid downgrades and liquidity risks being identified. Also, bonds of Lumen Technologies fell by over 25% due to its poor earnings forecast followed by its downgrade to B2 by Moody's. Ecuador's dollar bonds were down by over 20% during the month after partial results from its constitutional referendum showed that voters were planning to reject a series of proposals put forward by President Guillermo Lasso, with the preliminary results defying polls. Azul's dollar bonds also fell by over 15% after its downgrade to CCC- by Fitch. Among other notable losers were dollar bonds of Vedanta Resources that were affected by the government's involvement in trying to block the cash sale of its offshore zinc assets to Hindustan Zinc. Its dollar bonds were down as much as 15%. Also, Credit Suisse's perps dropped by over 12% in February after news broke out that the swiss financial markets regulator Finma was investigating the bank's involvement in market manipulation following the Chairman's comments in early December that outflows had halted.

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.