This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

March 20, 2023

Over the weekend, the Swiss government brokered a historic deal for UBS to takeover Credit Suisse in an all-stock deal worth CHF 3bn ($3.3bn). As part of the deal, the Swiss National Bank is offering CHF 100bn ($108bn) of liquidity assistance to UBS, while also granting a CHF 9bn ($9.7bn) guarantee for potential losses from assets that UBS is taking over. In a move that has shaken the AT1 bond (Term of the Day, explained below) market, the Swiss regulator has determined that Credit Suisse’s AT1s worth CHF 16bn ($17.3bn) will be completely written-off to zero (more details below).

This sparked a risk-off move with US Treasury yields falling across the board, back below 4% across the curve. The 2Y yield eased 29bp to 3.93% while the 10Y eased 11bp to 3.47%. Markets now price in a 64% probability of a 25bp hike at the FOMC meeting this Wednesday. US IG CDS spreads rose 5bp while HY CDS spreads jumped 26.7bp. US equity markets ended last week in the red with a 4.6% fall in the bank index dragging the S&P and Nasdaq lower by 1.1% and 0.5% respectively.

European equity markets closed in the red as well. European main and Crossover CDS spreads rose 2.6bp and 18.8bp respectively. Asia ex-Japan CDS spreads are largely flat while Asian equity markets have opened with a negative bias, led by Hang Seng down over 2.5%.

Keen to Learn About AT1s Following the Credit Suisse AT1 Write-Off?

Sign up for the course below.

.png)

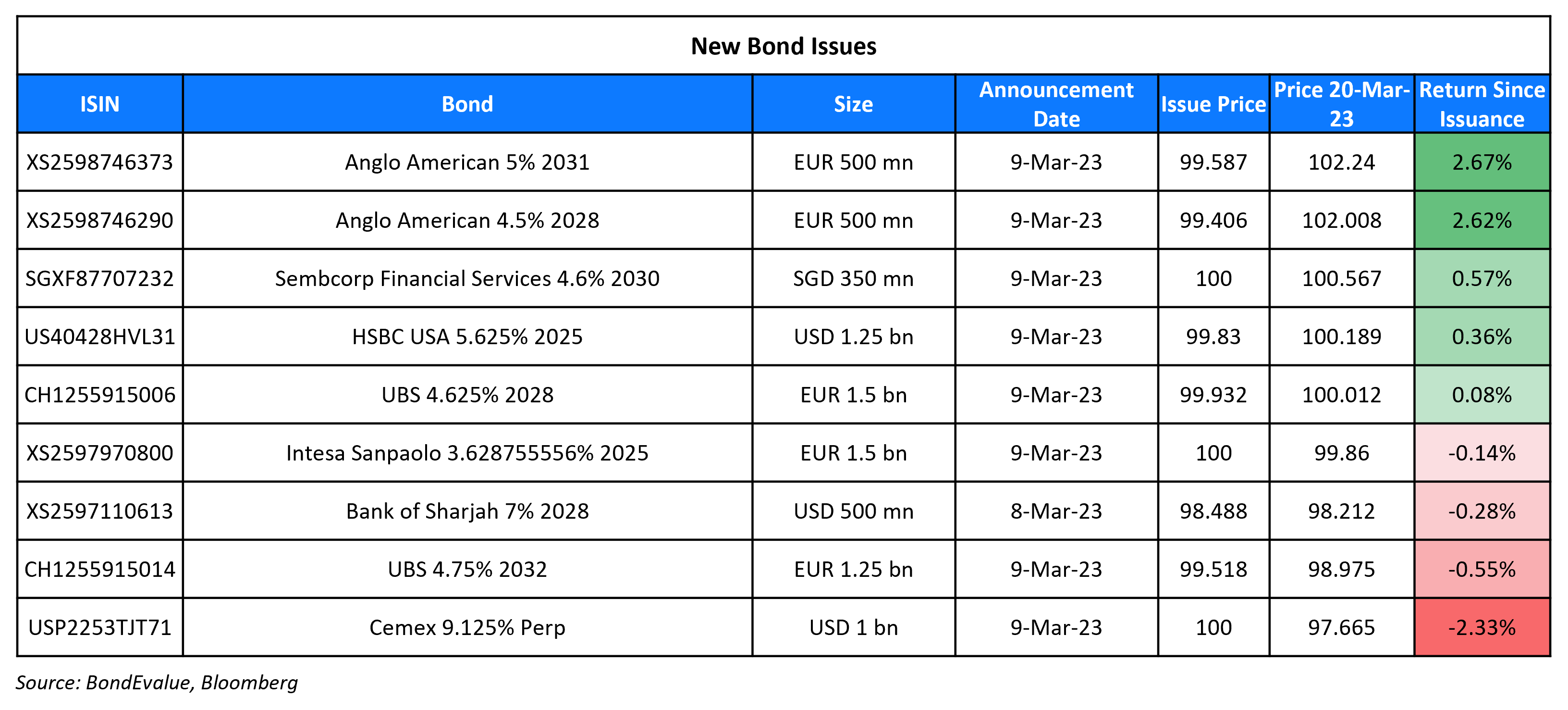

New Bond Issues

New Bonds Pipeline

- Shinhan Bank hires for $ senior bond

- REC hires for $ Long 5Y Green bond

- Qatar plans for $ bond

Rating Changes

-

Moody’s changes Saudi Arabia’s outlook to positive, affirms A1 ratings

-

Moody’s affirms Greece’s Ba3 ratings, changes outlook to positive from stable

-

Fitch Revises Braskem Idesa’s Outlook to Negative; Affirms Ratings at ‘BB-‘

Term of the Day: AT1 Bonds

Additional Tier 1 (AT1) bonds are hybrid securities issued by financial institutions to meet their regulatory capital requirements. AT1s typically carry a provision wherein the instruments can be fully or partially written-down or converted to equity if the issuing bank’s capital ratio falls below a certain threshold. This is why AT1s are also known as contingent convertibles (CoCos). The key characteristics of AT1 bonds are:

- They have a perpetual maturity with a call option

- They are subordinated in nature, and the first line of debt to incur losses

- They can be written-down or converted into equity on the occurrence of a “trigger event”

- Coupons are usually higher as compared to other debt by the issuer, to compensate investors for the higher risk AT1s carry. However, coupons can be discretionary in nature.

As part of Credit Suisse’s takeover by UBS, the former’s AT1s worth over $17bn have been written-off, the largest ever in the history of European AT1s.

For more on AT1s: The Complete Guide To AT1 Perpetual Bonds

Talking Heads

On the AT1s market following the Credit Suisse AT1 write-off

Luke Hickmore, investment director at abrdn Plc

“The AT1 market will be shut now for new issuance for a while. We will all be parsing which securities in AT1 space have a similar trigger to CS’s and which don’t, which banks need to issue AT1s and which don’t.”

John McClain, portfolio manager at Brandywine Global Investment Management

“It’s absolutely the right thing to do to prevent moral hazard from creeping into that part of the market. Those bonds were created for moments like this — similar to catastrophe bonds.”

Pauline Chrystal, a portfolio manager at Kapstream Capital in Sydney

“A lot of investors will want to reduce their exposure to the banking sector and if they can’t sell the weaker names, the next step will be to sell the next weakest that still has liquidity. Riskier securities will tend to sell off more, so either lower rated issuers or down the capital stack.”

On the expected move in US Treasuries

Jessica Ren, a fixed income strategist at Westpac Banking Corp.

“[Yields will continue to rise] but recalibration of risk sentiment should see some big swings as well and I don’t think we’ll settle into a new trading range until perhaps after this week’s FOMC. Price action will continue to be more sensitive than usual to headlines.”

Mohamed El-Erian, chief economic adviser at Allianz SE

“This is going to be pretty bumpy going forward. People are doing something that probably is not rational but is totally understandable — they’re moving deposits. That dynamic isn’t going to stop over night, neither are the losses that are being incurred.”

Todd Baker, a senior fellow at Columbia University’s Richard Paul Richman Center for Business, Law and Public Policy

The biggest open question is First Republic, which suffered a run after being somewhat unfairly linked to Silicon Valley Bank and Signature Bank. I am expecting a private capital infusion or an M&A deal soon there so that the bank can hold onto primary banking relationships with its core base of wealth individuals and their businesses.”

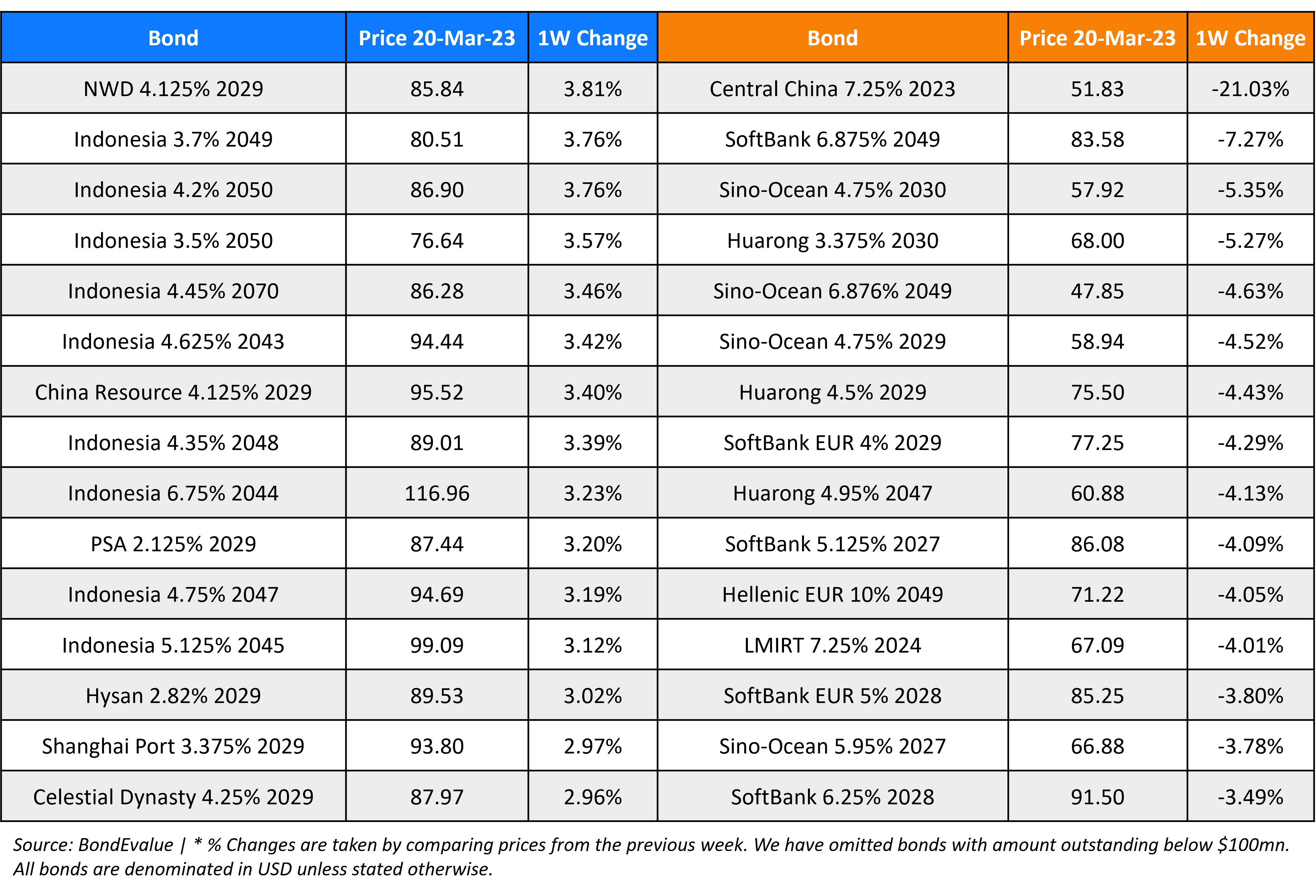

Top Gainers & Losers – 20-March-23*

Go back to Latest bond Market News

Related Posts:

NWD’s China Unit Planning $732mn Project in Guangzhou

August 26, 2021

SBI Reports 62% Quarterly Profit Jump

February 7, 2022

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.