This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Treasuries Rally with 2Y Yield Down 13bp; Macro; Rating Changes; New Issues; Talking Heads; Gainers and Losers

April 5, 2023

US Treasuries continued to rally across the curve with the 2Y and 5Y yields down by 11-13bp. First, US JOLTS Job Openings dropped by 623k to 9.9mn in February, the lowest since May 2021, and below estimates of 10.5mn, suggesting a cooling labor market. Secondly, in a letter to shareholders, Jamie Dimon, the CEO of JPMorgan Chase said that the ongoing banking crisis is “not yet over” and that its impact will be felt for years. He also remarked that the “market’s odds of a recession have increased… it is not clear when this current crisis will end. It has provoked lots of jitters in the market and will clearly cause some tightening of financial conditions”. Bank equities saw a sell-off, with the S&P Bank Index falling 1.9%. The S&P and Nasdaq ended lower on Tuesday, down by 0.6% and 0.5% respectively.

The peak Fed funds rate also fell by 4bp to 4.94% for the May meeting. On the back of the above, CME maximum probabilities now show a 58% chance of a status quo at the May 2023 FOMC meeting as compared to a 58% chance of a 25bp hike yesterday. US IG and HY CDS spreads widened 2.2bp and 11bp respectively.

European equity markets ended mixed. European main CDS spreads widened by 2.1bp and Crossover spreads were 10.6bp wider. Asia ex-Japan CDS spreads widened by 2.7bp. Asian equity markets have mixed this morning.

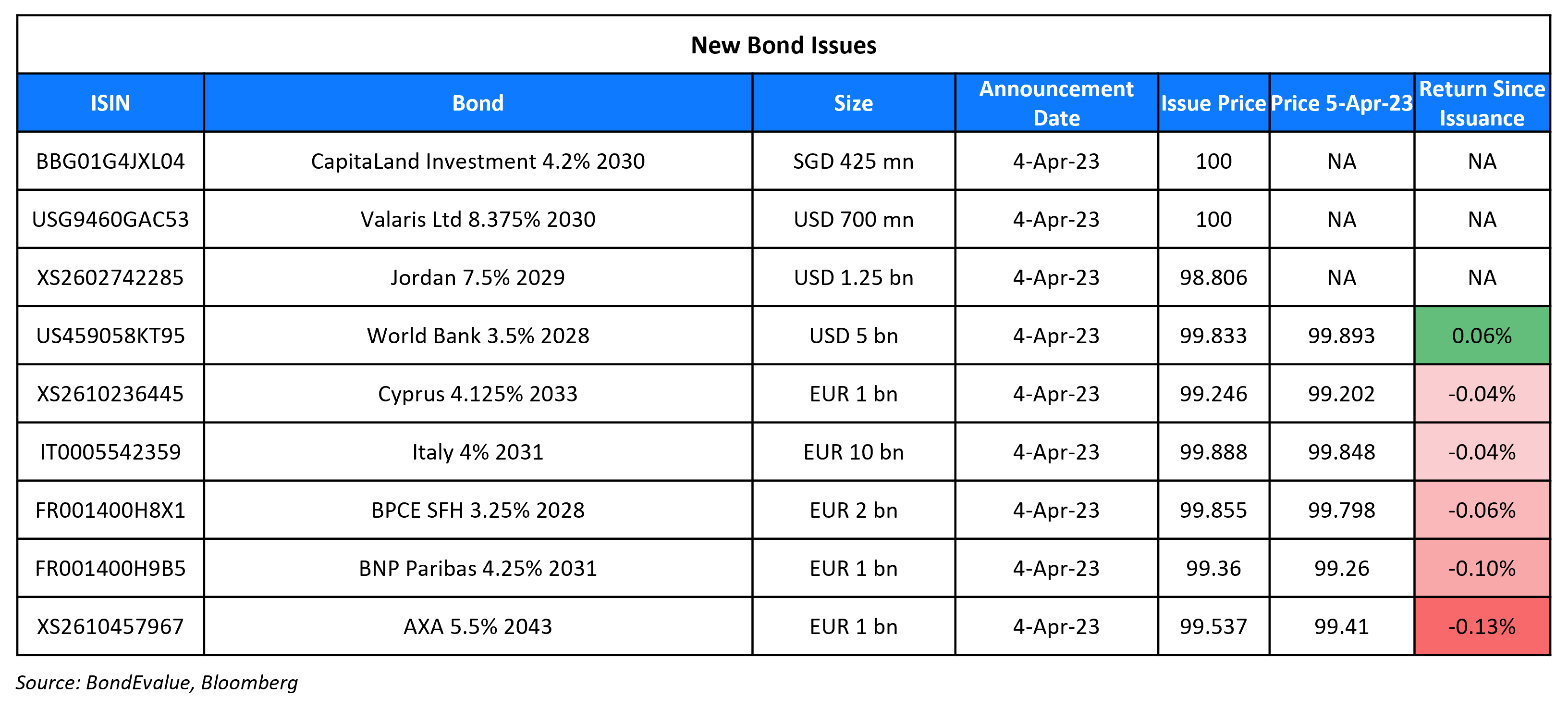

New Bond Issues

BNP Paribas raised €1bn via a 8NC7 Green bond at a yield of 4.358%, 23bp inside initial guidance of MS+160bp area. The senior non-preferred bonds have expected ratings of Baa1/A-/A+, and received orders over €1.85bn, 1.9x issue size. Proceeds will be used to (re)finance Eligible Green Assets. The new bonds are priced in in-line with the issuer’s existing 0.875% conventional 2030s that yield 4.3%.

Jordan raised $1.25bn via a Long 5Y bond at a yield of 7.75%, 37.5bp inside initial guidance of 8.125% area. The bonds are rated B1/B+. Proceeds from the senior unsecured notes will be used for permitted purposes under the Jordanian Public Debt Management Law. The new bonds are priced at a new issue premium of 34bp to its existing 7.75% 2028s that yield 7.41%.

CapitaLand Investment raised S$425mn via a 7Y bond at a yield of 4.2%, a spread of SORA+136.9bp and 25bp inside initial guidance of 4.45% area. Proceeds from the senior unsecured notes will be used to refinance existing borrowings, finance investments, and for general working purposes. The bonds are issued by CLI Treasury and guaranteed by CapitaLand Investment. CLI Treasury last tapped the SGD market in 2022 with a S$400mn issuance of its 3.33% 2027s.

AXA raised €1bn via a 20.25NC10.25 Tier 2 bond at a yield of 5.564%, 35bp inside initial guidance of MS+295bp area. The subordinated bonds have expected ratings of A1/A+, and received orders over €4.6bn, 4.6x issue size.

New Bonds Pipeline

- Kookmin Bank hires for $ 3Y and/or 5Y bond

Rating Changes

- Moody’s upgrades Bombardier’s CFR to B2; outlook stable

- BankMuscat S.A.O.G. Outlook Revised to Positive On Improving Macroeconomic Conditions; ‘BB/B’ Ratings Affirmed

- Fitch Downgrades Rogers’ IDR to ‘BBB-‘; Outlook Stable

Term of the Day

Grandfathered Bond

Grandfathered bonds refer to a European class of bonds issued prior to March 1, 2001 that were exempted from retention tax payment. A retention tax is a tax that is automatically withheld or paid directly to the government and became effective on July 1, 2005. Since these bonds were issued much earlier, the old rules of not paying retention taxes continued to apply onto the bonds, thus making it “grandfathered”.

HSBC has decided to redeem $1.95bn of its discos or discounted floating perps issued in 1985-1986 that were grandfathered as Tier 2 capital until 2025.

Talking Heads

On Bond Meltdowns Hiding in Plain Sight Burning EM Buyers

Gary Kleiman, senior partner at Kleiman International Consultants

“This is a cautionary tale. The signs have been simmering all along”

Patrick Esteruelas, head of research at Emso Asset Management

“Lasso’s political capital has been on a steady decline since the protests broke out in June last year, with every political actor in Ecuador smelling blood since… it’s hard to see any positive catalysts that will push these prices higher”

On Pimco Saying It Favors ‘Strong Bonds’ Amid Rising Recession Risks

“Not tightening further is different than normalizing or even easing policy, which will likely require inflation falling toward target levels… bonds appear poised to exhibit more of their traditional qualities of diversification and capital preservation, with the potential for upside price performance in the event of further economic deterioration… banking stress “reinforces our cautious approach toward corporate credit, particularly lower-rated areas such as senior secured bank loans… “have a preference for structured, securitized products backed by collateral assets”

On Investors Unloading Saudi Arabian Bonds After Surprise Prouction Cut

Todd Schubert, Dubai-based head of fixed-income research at Bank of Singapore

“It’s largely because of valuations. Spreads are not compelling relative to corporates from similarly rated countries in Asia such as Japan or Korea.”

Abdul Kadir Hussain, head of fixed-income asset management at Arqaam Capital.

“Given the fact that regional spreads are already tighter than global EM, I would not expect huge outperformance. This won’t change the fundamental dynamics of GCC bonds, which will remain the ‘safe haven’ trade”

On Trading Volatility Being the New Reality for Bond Investors

Vineer Bhansali, founder of LongTail Alpha

“I’m not willing to take much duration risk because I don’t really know if we fall into an abyss and rates rally, or everything stabilizes. What I am primarily trading is the yield curve, wagering on steepening”

Darren Davy of Omega Family Office

“For the next 12 to 18 months, we are going to go through a very interesting global fixed-income transition. In this type of volatility environment, you have to be very, very careful. Overall, there’s more a story now about a continued normalizing of yield curves and the risk to duration – which should have a premium”

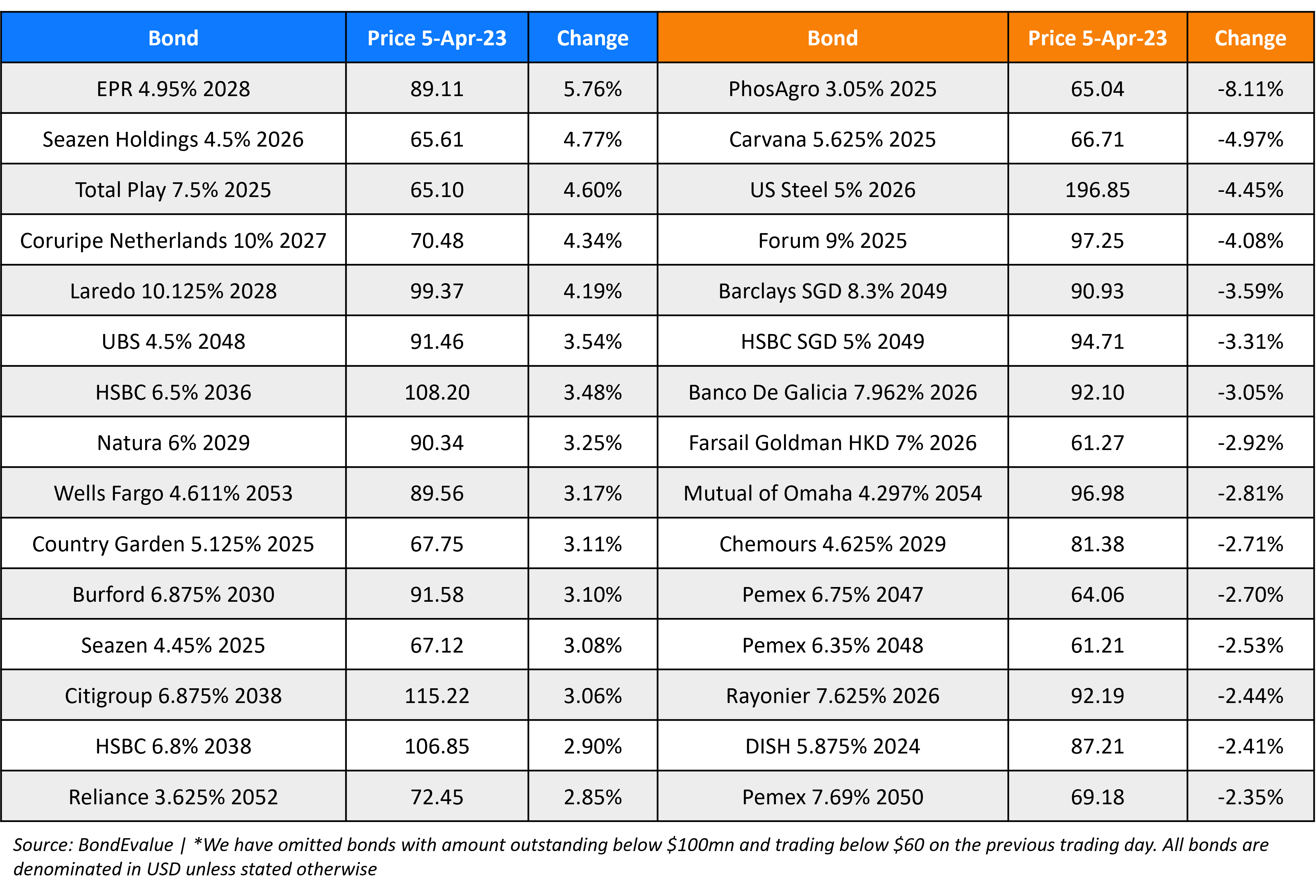

Top Gainers & Losers – 05-April-23*

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.