This site uses cookies to provide you with a great user experience. By using BondbloX, you accept our use of cookies.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Bond Market News

Quarter End Update: 74% Dollar Bonds Trade Lower in Q1; HY Outperforms IG

April 1, 2021

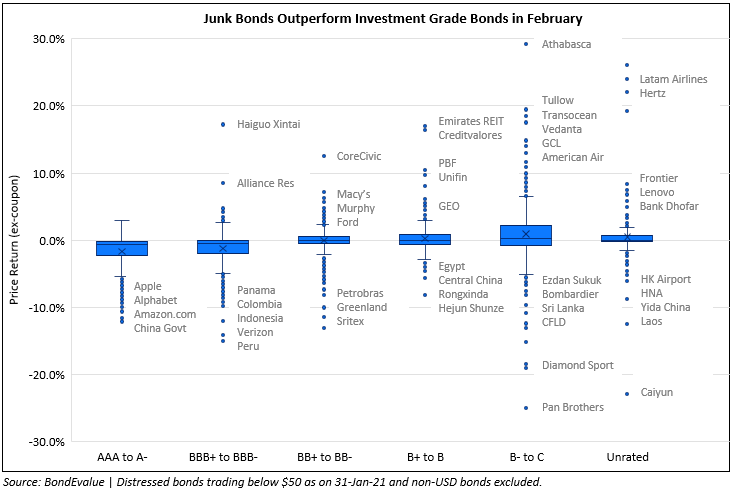

The first quarter of 2021 was a gloomy one for investors as 74% of dollar bonds in our universe delivered a negative price return (ex-coupon). The month of March saw a continuation of February’s disappointing run in bond markets with 82% of dollar bonds delivering negative returns.

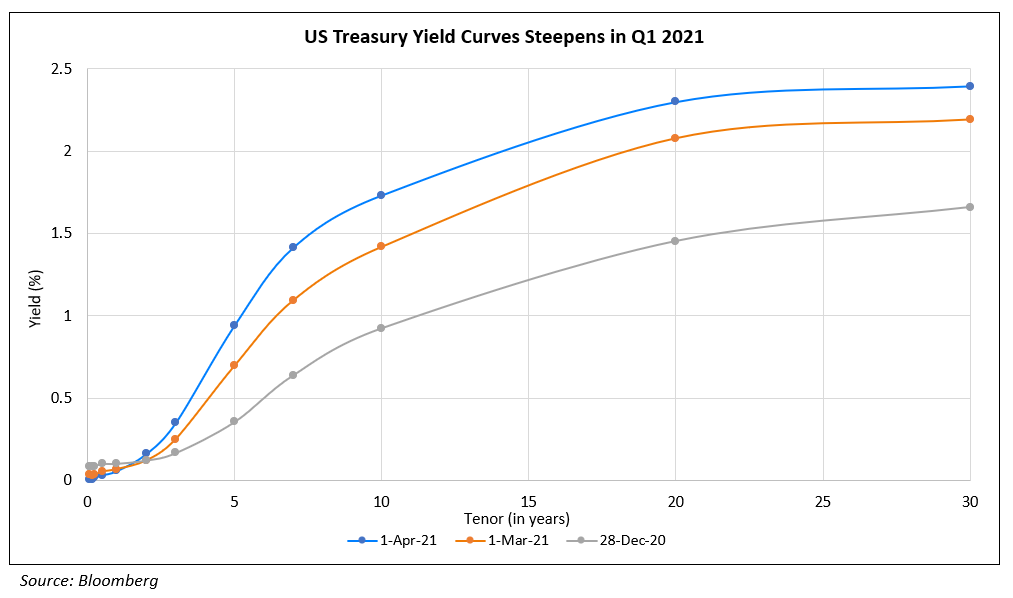

Investment Grade bonds (IG) saw yet another month of underperformance vs. High Yield bonds (HY) with one factor being the continued sell-off in US Treasuries that led to a ~25bp rise in yields for both the 10Y and 30Y, currently at 1.74% and 2.40% respectively resulting in a steeper yield curve compared to 2020-end. Overall in Q1, only 17% of IG bonds saw a positive price return, worse than even Q1 2020 when assets sold-off across the board in late March leading to 24% of IG bonds delivering positive price returns. HY on the other hand fared better with 39% delivering a positive return in Q1 2021, far more than the 2% bonds that traded in the green in Q1 2020.

Issuance Volume

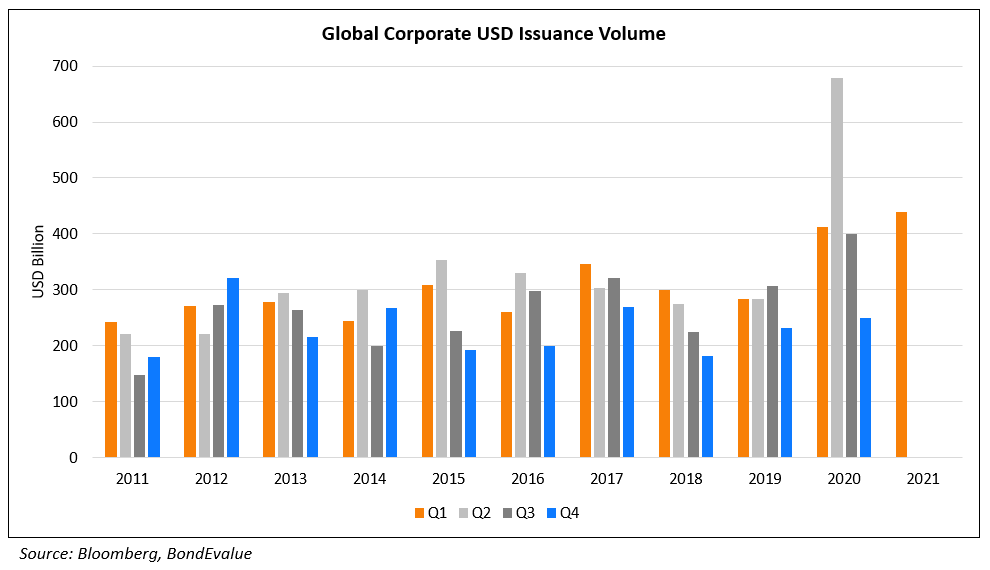

Global corporate dollar issuance volume stood at $439bn for Q1, up 7% vs. Q1 2020. For the month of March, issuance volume stood at $201bn, down 15% vs. last March’s issuance of $236bn and 63% higher than February which was at $115.3bn.

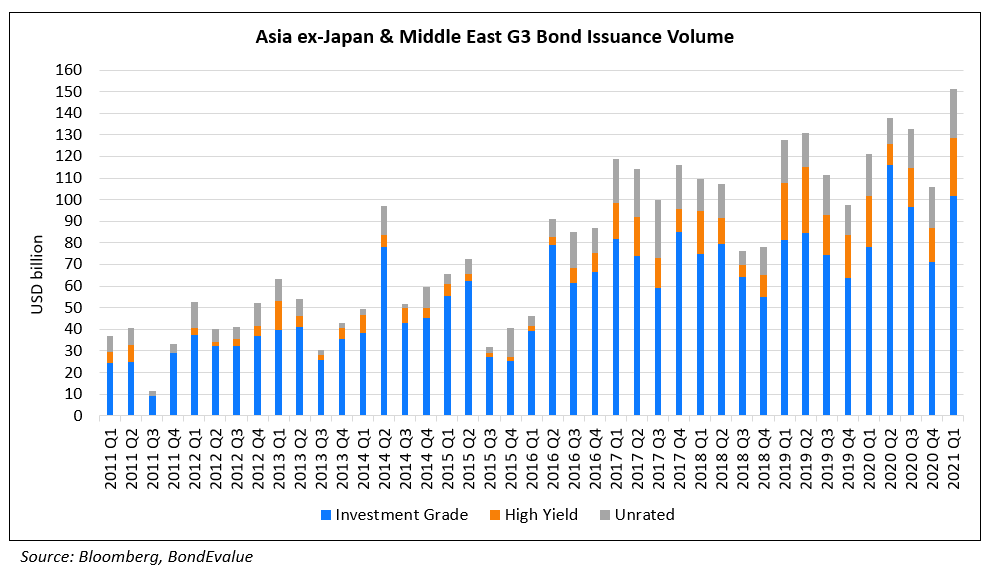

Asia ex-Japan G3 currency Q1 issuance volume stood at 151bn, up 25% vs. Q1 2020. For the month of March, issuance volume stood at $40bn vs. last March’s issuance of $13bn as primary markets were spooked by the March mayhem last year.

Looking at the issuance across industries, the table below shows volumes being dominated primarily by sovereigns and banks, both globally and in the APAC & ME region.

Largest Deals

The largest corporate dollar issuance during the quarter was by Verizon raising $25bn via a jumbo nine-part offering . This was followed by Apple’s $14bn six-trancher in early Feb which surpassed 7-Eleven’s $10.95bn offering just a week prior. Other notable deals were that of Boeing that raised $9.825bn via a three-part offering, which offered new issue premiums of 24-45bp on all the three tranches over its older bonds at the time of issuance, Wells Fargo’s $3.51bn 3.9% Perp and Carnival’s 5.75% 2027 amounting to $3.5bn.

Top Gainers & Losers

Most notable among the gainers was Hertz’s bonds, which rallied sharply led by its 7.125% 2026s from distressed levels of 52 to 99 currently on the back of a $4.2bn investment lifeline by Knighthead Capital Management after having filed for bankruptcy protection in May 2020. Prospects of recovering air travel saw bonds of LatAm Airlines and GoI. LatAm noted that November 2020 passenger load stood at 74%, the highest in the world vs. the industry average of 58%. Other notable gainers included WeWork whose bonds jumped on news of the co-working company going public via a SPAC named BowX.

The losers list was primarily dominated by Asian players with Indonesian Garment maker Sritex seeing its dollar bonds nosedive after getting downgraded by Moody’s in March. Also making it to the list were Chinese real estate developer China Fortune Land Development (CFLD), which saw a spate of downgrades, a severe liquidity crunch leading to CFLD asking for an extension on its bonds that matured in end-February and news of increasing debt overdue. Another Chinese real estate developer Yuzhou Properties also saw its bonds take a beating in March after getting downgraded to Ba3 with a negative outlook and guiding for a 97% drop in earnings.

Go back to Latest bond Market News

Related Posts:

BondbloX is regulated by the Monetary Authority of Singapore as a Recognised Market Operator ("RMO") and exempted from Section 49(1) of the Securities and Futures Act (Cap. 289) ("SFA") under Section 49(7) of the SFA.